Macro and

Equity Market

Outlook

Equity Market

Outlook

GLOBAL MACRO & MARKETS

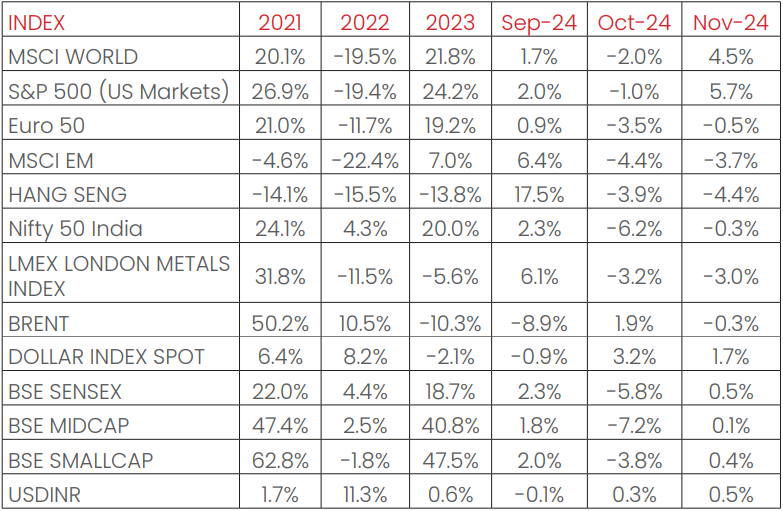

India’s NSE NIFTY index ended almost flat in November 2024 (-0.3%).

Among major global indices, the S&P500 (+5.7%) rallied post the

United States (US) Federal election results, with the Euro 50 (-0.5%),

and the Japanese NIKKEI (-2.2%) ended the month, November 2024

with negative returns. The Morgan Stanley Capital International

(MSCI) World (+4.5%) bucked the trend on a sequential basis,

ending the month, November 2024 in green aided by performance

of the largest market, the United States (US). Performance was

largely negative among Emerging Markets (EM) indices, with the

Morgan Stanley Capital International Emerging Markets (MSCI EM),

the Hang Seng (Hong Kong), the BOVESPA Brazil (BVSP) recording

sequential returns of (-4.4%), (-3.7%), and (-3.1%) respectively.

The London Metals Exchange (LME) Metals Index fell by (-3.0%) in

November 2024, driven by weak global demand and limited

recovery in largest consumer market, in China. The West Texas

Intermediate (WTI) and Brent Crude fell MoM, by (-1.8%) and (-0.3%),

respectively, as markets remained cautious given geo-political

tensions.

The Dollar index appreciated by (+1.7%) through November 2024,

with the US Dollar (USD) losing vis-à-vis Emerging Market (EM)

currencies (-2.4%) and appreciating against the Indian Rupee (INR)

on the spot market (+0.5%). India 10Y G-Sec yields fell by (-10 bps),

while US 10Y G-Sec yields fell by (-10 bps), and the German Bund

yield fell by (-30 bps), with rates settling at 6.74%, 4.16% and 2.08%

respectively, as hopes of monetary easing remain.

Domestic Macro & Markets

The BSE SENSEX (+0.5%) rose in November 2024, in contrast to the

NSE NIFTY index. The BSE Mid-cap index and the BSE Small-Cap

index underperformed the BSE SENSEX, rising by (+0.1%), and +0.4%

over the month respectively. Sector-wise, Information Technology

(IT), Tech and Consumer Durables were the top 3 performers over

the month, November 2024 clocking (+5.8%), (+4.9%), and (+3.0%),

respectively.

Net Foreign Institutional Investors (FII) flows into equities remained

negative for November 2024 (-$ 2.5 Bn, following $ -11.2 Bn in

October 2024). The Domestic Institutional Investors (DIIs) remained

net buyers of Indian equities in November 2024 (+$4.5 Bn, from

+$12.8 Bn last month, October 2024). In Calendar Year (CY2024), Net

Foreign Institutional Flows (FII) Flows stood at (-$2.0 Bn), while net

Domestic Institutional Investors (DII) investments in the cash

markets stood at (+$58.2 Bn), outpacing the Foreign Institutional

Investors (FII) investments.

India's high frequency data update:

Record levels of Goods and Services Tax (GST) collections, stable retail

inflation, softer input inflation, rising core sector outputs, and elevated

credit growth augurs well for the Indian economy.

Purchasing Managers’ Index Manufacturing PMI:

India’s Manufacturing Purchasing Managers’ (PMI) in November 2024

slowed month on month to 56.5 (vs 57.5 in October 2024), remaining

in expansion zone (>50) for the 40th straight month. The slowdown

was countered by an acceleration in exports and sales, but with the

rate of output expansion slowing.

Goods and Services Tax (GST) Collection:

Gross collections of INR 1.82 Tn (+8.5% YoY) in November 2024

concluded the thirty third consecutive month of collections over

the INR 1.4 Tn mark, following previous record collections of INR 2.1 Tn

in April 2024. Rising compliance, higher output prices, festive

season demand, rising collections from imports and domestic

transaction volume uptick has driven elevated tax collections.

Core Sector Production:

The index of eight core sector industries grew by (+3.1%) YoY in

October 2024, against a (+2.4%) growth in September 2024, as an

unfavourable base effect came into play. 7 out of eight constituent

segments grew YoY, driven by Coal production (+7.8% YoY).

Industrial Production:

Factory output growth as measured by the Index of Industrial

Production (IIP) accelerated MoM to (+3.1%) in September 2024, vs

a de-growth of (-0.1%) YoY in August 2024, driven by positive, and

YoY growths in 3 of 3 major sectors- Manufacturing, Mining,

Electricity.

Credit growth:

Scheduled Commercial Bank Credit growth reached (+11.15%) YoY

as of 15th November 2024 against a YoY growth of (+20.64%) as

observed on 17th November 2023, as a strong base effect came to

play post the merger of Housing Development Finance

Corporation (HDFC and HDFC Bank).

Inflation:

October 2024 Consumer Price Index (CPI) inflation rate

accelerated sharply MoM to (+6.21%), up from 5.49% in July 2024.

Food inflation came in at a faster pace, at (+10.87%). The Wholesale

Price Index (WPI) inflation accelerated sequentially in October 2024,

with the print at (+2.36%), 52 bps up from September 2024.

Trade Deficit:

Indian Merchandise Exports rose by (+17.26%) YoY to $39.2 Bn in

October 2024, while Imports rose by (+3.88%) YoY to $66.34 Bn.

Merchandise trade deficit widened by (-10.81%) YoY to $27.14 Bn.

Events to watch out for in December 2024:

The United States (US) Policy Shift:

The threat of raising tariffs on foreign goods being imported into

the USA remains, as the administration changes, which has

implications on inflation and global trade. This remains a key

monitorable for global demand and price oriented companies

and markets in general.

The Federal Open Market Committee (FOMC) Meeting:

The Federal Open Market Committee (FOMC) meets on December

18th ,2024 to discuss further rate cuts, after cutting rates in the last

2 meetings in September 2024 and November 2024. The policy rate

stands at 4.5%-4.75%, and expectations of a rate cut of 25 bps in

December 2024 are priced in by the markets. Data flow, especially

labour market and inflation may drive further changes in policy

rates.

Other things to watch out for:

Festive season demand, Oil market Volatility, and Central

Government’s Capex stance, The Goods and Services Tax (GST)

council meeting remain key events for markets to watch out for.

Monthly Performance for Key Indices:

Source: Bloomberg

.*Calendar year returns.

Note:Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Note:Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Market View

November 2024 witnessed slew of global and domestic

developments leading to a relatively higher market swings. In the

United States (US) with new leadership taking shape early next

year material policy shifts, if any needs to be monitored.

On the domestic space the recent state election results can give a

thrust to policy continuity. The Gross Domestic Product (GDP) for

Q2 FY’25 came in at 7 quarter low of 5.4% YoY due to multiple

factors like weather vagaries, slowdown in urban consumption

and lower government spending etc. However, we expect some of

these challenges to be behind supported by higher government

spending, festive season demand and robust Kharif and Rabi

season.

From corporate earnings perspective we may believe that the

worst of the earnings downgrades is over and 2HFY25 may see a

minimal earnings downgrade. While overall consumption is weak

the premiumisation trend remains strong. Some of the global

demand-oriented business like Information Technology (IT)

services and metals have minimal risk of earnings downgrades.

Post this fall large cap valuations are closer to long term averages

while the mid and small caps despite the recent correction trade

at premium supported by strong domestic flows.

Considering the recent geopolitical events especially the

uncertain policy environment, volatility in currency markets,

relative India valuations the market volatility may higher than

usual in the near term. Accordingly, investors can consider well

diversified large cap-oriented strategies like Large/Flexi/Multi Cap

appear over the medium term.

Investors seeking better downside protection may consider asset

allocation products like Multi Asset Allocation, Dynamic Equity ,etc.

Long term investors with appropriate risk appetite can consider

Mid and Small Cap allocations in staggered manner through the

systematic route.

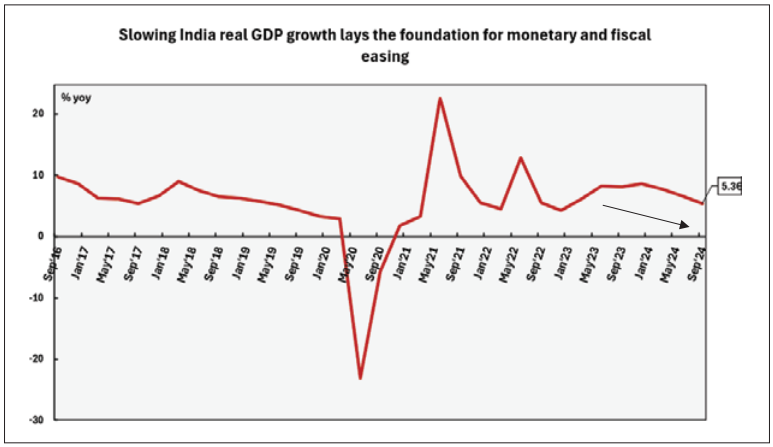

Chart of the Month:

India’s Q3 Calendar Year (CY24) real Gross Domestic Product

(GDP) growth dropped to a seven-quarter low of 5.4%

year-over-year (yoy) vs. 6.7% yoy in Q2. Private consumption

expenditure and fixed investment growth declined to 6.0% yoy and

5.4% yoy respectively. Agriculture sector growth increased to a

five-quarter high of 3.5% yoy and bodes well for the rural recovery,

while both manufacturing and services sectors’ growth

disappointed. 1HFY25 growth came in worse than expectations

partly due to one off factor and 2HFY25 growth is likely to be better.

However, market has started to expect preponement of monetary

easing alongside increased Government spending to spur growth.

Source:

NIMF Research, CEIC

Disclaimer:

The information herein above is meant only for general reading purposes and the views being expressed

only constitute

opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide

for the readers.

The document has been prepared on the basis of publicly available information, internally developed

data and other

sources believed to be reliable. The sponsors, the Investment Manager, the Trustee or any of their

directors, employees,

Associates or representatives (‘entities & their Associate”) do not assume any responsibility for, or

warrant the accuracy,

completeness, adequacy and reliability of such information. Recipients of this information are advised

to rely on their own

analysis, interpretations & investigations. Readers are also advised to seek independent professional

advice in order to

arrive at an informed investment decision. Entities & their associates including persons involved in

the preparation or

issuance of this material, shall not be liable in any way for any direct, indirect, special,

incidental, consequential, punitive,

or exemplary damages, including on account of lost profits arising from the information contained in

this material.

Recipient alone shall be fully responsible for any decision taken on the basis of this document.

The sectors mentioned are not a recommendation to buy/sell in the said sectors. Details mentioned

above are for

information purpose only.