Macro and

Equity Market

Outlook

Equity Market

Outlook

Global Macro & Markets

2022 started on a volatile note as the US Fed

signaled faster tightening of monetary policy. US

10Y interest rates rose 27 bps while the Dollar index

strengthened 0.9% over the month. MSCI World

was down 5.3%, in line with the fall in S&P 500

(-5.3%). Euro-50 and Japanese Nikkei lost 2.9% and

6.2% respectively. NASDAQ composite, however, fell

almost 9% over the month as Tech stocks globally

stood to be the biggest losers of the Fed’s faster

than expected rate hikes. MSCI EM was down 1.9%.

BOVESPA Brazil rebounded to gain 7% while MOEX

Russia lost 6.8% MoM. India’s NIFTY (-0.1%)

remained flat MoM. LME Metals index stayed

resilient with 1.9%m/m gains. Brent Crude, standing

the single largest beneficiary of the geopolitical

tensions between Russia and Ukraine, gained

17.3%m/m.

Domestic Macro & Markets

Sensex rose about 5% by January 17, only to give it all back during

the rest of the month. Broader market marginally underperformed

over the month. BSE Midcap index and BSE Smallcap index were

both down 1.4% and 0.8% respectively. Among sector indices,

Utilities (+14%), Financials (+3%) and Discretionary (+3%)

outperformed the index while IT (-9%), HealthCare (-8%) and

Staples (-5%) lagged the most. Market breadth improved in

January with 54% of BSE 200 stocks trading above their respective

200-day moving averages. FPIs sold US$3.8 bn of Indian equities in

the secondary market while DIIs bought US$2.5 bn.

India's high frequency data update:

Positive momentum in GST collections, manufacturing activity and

exports bode well for near term economic rebound after mild

disruption caused by the rapid spread of the Omicron variant.

Manufacturing PMI:

Manufacturing PMI continued to remain expansionary at 54 in

January'22, albeit slowly compared to 55.5 in December'21.

GST Collection:

With collections at INR 1.41 Tn (+15% YoY) in January'22, the

Government recorded highest ever collections since the inception

of the GST in July 2017.

Power consumption:

Power consumption in the month of January'22 was 1.1% higher

than January'21 and 5.9% higher than the consumption in

January'20.

Core sector production:

Core sector production rose 3.8% YoY in December'21 as against a

YoY rise of 3.4% in November'21 and rise of 0.4% in December last

year.

Industrial Production:

Manufacturing IIP rose 0.9% in November'21 vs dip of 1.6% in

November last year.

Credit growth:

Credit growth inched up to 8% YoY as of 14-Jan'22 against YoY

growth of 6.4% as observed on 15-Jan 2021. Aggregate deposit

growth remained flat at 9.3% YoY.

Inflation:

CPI inflation in December'21 shot up to 5.59% from 4.91% on the back

of elevated fuel and light inflation (+11%) and core inflation (+6.2%).

WPI inflation moderated to 13.6%.

Trade Deficit:

December'21 trade deficit came at US$22 bn as compared to

US$22.9 bn in November'21. Exports increased 37% YoY to US$37.3 bn

while imports increased by 38% YoY to $59.3 bn.

Balance of Payments (BOP):

The current account registered a deficit of US$9.6 bn (1.3% of GDP)

in 2QFY22 against a surplus of US$6.5 bn in 1QFY22 (0.9% of GDP)

and surplus of US$15.3 bn (2.4% of GDP) in 2QFY21. The deficit was led

by a widening of the trade deficit to US$44.4 bn (1QFY22: US$30.7

bn) and an increase in net investment income outflow of US$10 bn

(US$7 bn in 1QFY22).

Union Budget:

The budget maintained a pro-growth bias with transparent and

credible set of assumptions for tax revenue growth as well as

expenditure plans. Capital expenditure growth is pegged at

24.5%yoy in FY23, which will take central govt’s capex-to-GDP to an

18 year high of 2.9%. From extension of credit guarantee scheme for

SMEs and MSMEs to touching upon battery swap policy for EVs and

incentivizing solar cell manufacturing in India, focus has been on

an all-inclusive secular growth of the economy. Fiscal

consolidation along with improvement in quality of spending were

key highlights of the Union budget.

Market View

Domestic economic recovery is likely to be in line with expectations

supported by:

- Robust government capital spending, nascent signs of private corporate capex recovery, and revival in housing investment

- Strong Urban discretionary Consumption driven by pent up demand

- Healthy Exports

We believe broad based recovery in the markets will continue (with

volatility) as the economy revives and earnings growth is expected

to sustain on continued macro recovery. Technology, China+1 and

Domestic recovery/outdoor consumption may be key themes

dominating the market. Major risks to our view are higher Inflation,

Oil price, New virus variants.

We believe all three market cap segments (Large, Mid and Small)

offer similar risk reward, making a case for diversified strategies with

investments across market caps. Conservative investors seeking

equity exposure with lower volatility may consider asset allocation

strategies like Balanced Advantage etc which manage equity

allocations dynamically.

Note: The sectors mentioned are not a recommendation to buy/sell in the

said sectors. The schemes may or may not have future

position in the said sectors. For complete details on Holdings & Sectors of NIMF

schemes, please visit website mf.nipponindiaim.com;

Past performance may or may not be sustained in future

Past performance may or may not be sustained in future

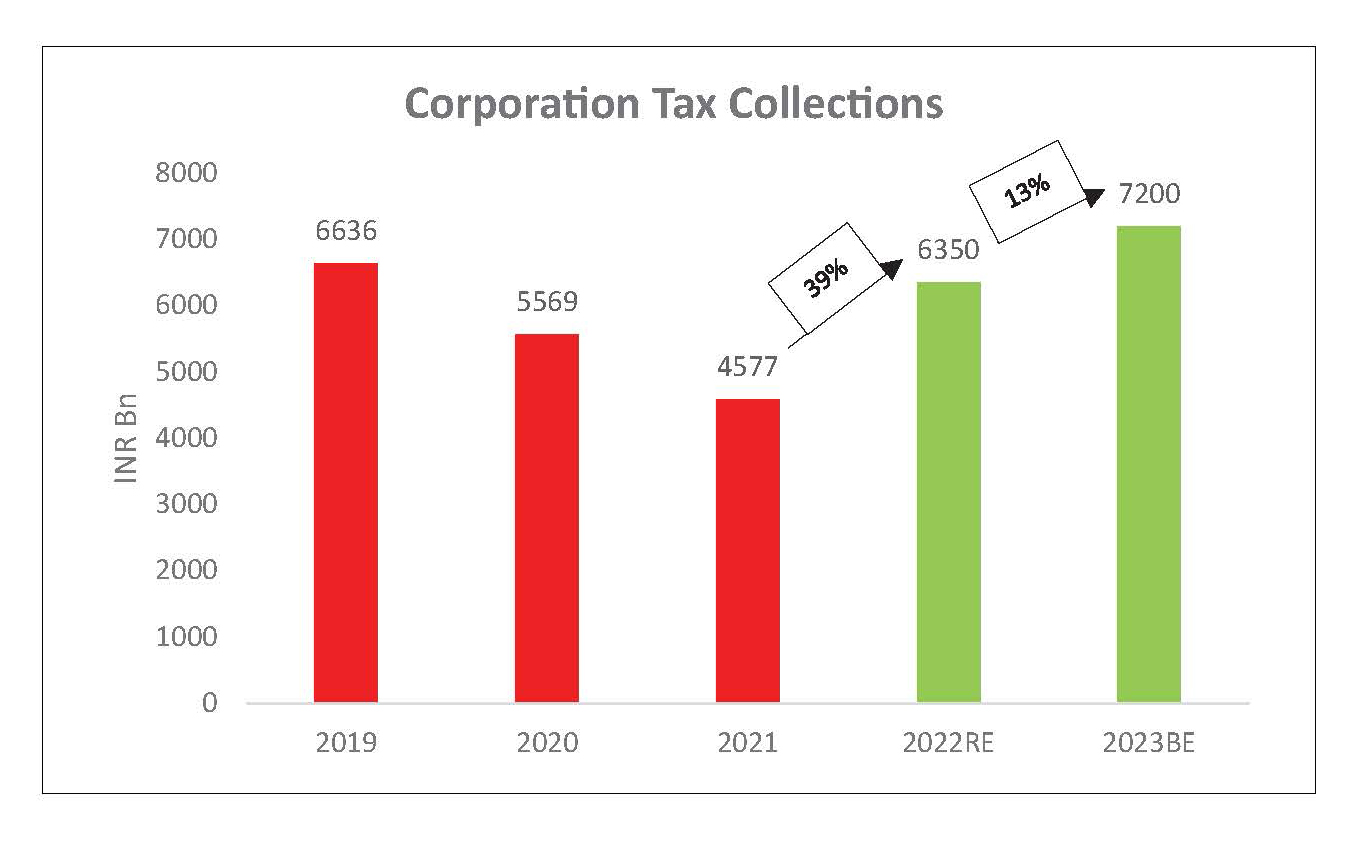

Chart of the month :

Rise in corporate tax collection by 39% and 13% in FY22 and FY23

basis budget estimates is indicative of sustained rise in Corporate

Profits to GDP ratio for India.

Common Source:

Budget Documents, Nippon India Mutual Fund Research,

Bloomberg

Disclaimer:The views expressed herein are based on publicly available

information and other sources believed to be

reliable. It is issued for information purposes only and is not an offer to sell or a

solicitation to buy/sell any mutual fund

units/securities. It should be noted that the analysis, opinions, views expressed in the

document are based on the Budget

proposals presented by the Honourable Finance Minister in the Parliament on Feb 1, 2022

and the said Budget proposals

may change or may be different at the time the Budget is passed by the Parliament and

notified by the Government. The

information contained in this document is for general purposes only and not a complete

disclosure of every material fact

of Indian Budget. For a detailed study, please refer to the budget documents available

on http://www.indiabudget.gov.in

The information herein above is meant only for general reading purposes and the views

being expressed only constitute

opinions and therefore cannot be considered as guidelines, recommendations or as a

professional guide for the readers.

The document has been prepared on the basis of publicly available information,

internally developed data and other

sources believed to be reliable. The sponsors, the Investment Manager, the Trustee or

any of their directors, employees,

Associates or representatives (‘entities & their Associate”) do not assume any

responsibility for, or warrant the accuracy,

completeness, adequacy and reliability of such information. Recipients of this

information are advised to rely on their own

analysis, interpretations & investigations. Readers are also advised to seek independent

professional advice in order to

arrive at an informed investment decision. Entities & their associates including persons

involved in the preparation or

issuance of this material, shall not be liable in any way for any direct, indirect,

special, incidental, consequential, punitive or

exemplary damages, including on account of lost profits arising from the information

contained in this material. Recipient

alone shall be fully responsible for any decision taken on the basis of this

document.