Macro and

Equity Market

Outlook

Equity Market

Outlook

GLOBAL MACRO & MARKETS

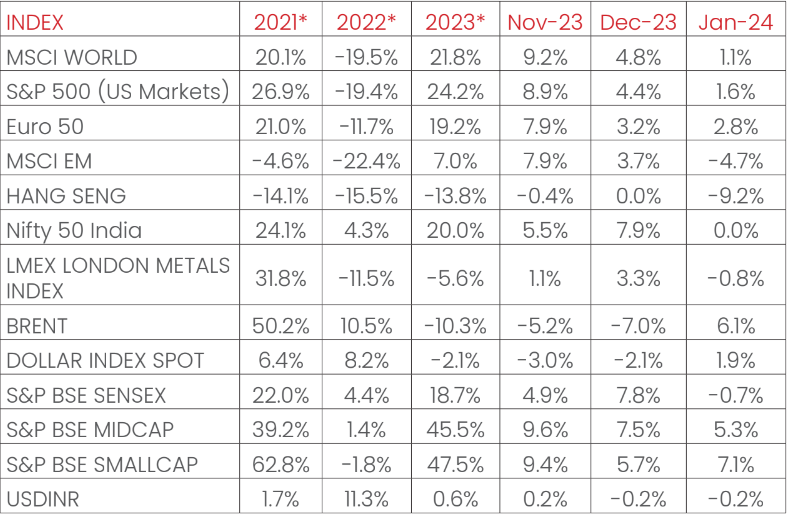

India’s NIFTY index ended the month flat in January 2024. The

S&P500 (+1.6%), the Euro 50 (+2.8%), the Morgan Stanley

Capital International World (MSCI) (+1.1%), and the Japanese

NIKKEI (+8.4%) rounded a positive month for major global

indices. Among Emerging Market (EM) indices, the Morgan

Stanley Capital International (MSCI) Emerging Markets, the

HANG SENG (Hong Kong) and the BOVESPA (BVSP) Brazil were all

down in January 2024 by -4.7%, -9.2% and -4.8%, respectively.

The Moscow Exchange (MOEX) Russia Index was up +3.7%, bucking

the trend for EMs.

London Metal Exchange (LME) remained flat (-0.8%) in January

2024, as top consumer China’s demand outlook remained tepid in

response to the property sector crisis in the country. West

Texas Intermediate (WTI) and Brent Crude rebounded over the

month, by +5.9% and +6.1% respectively as global oil markets

remained volatile based on the sustenance of The Organization

of the Petroleum Exporting Countries (OPEC+) production caps

and the situation in the Red Sea.

The US Dollar index strengthened by +1.9% through January

2024, with the US Dollar depreciating by -1.8% vis-à-vis

Emerging Market currencies and depreciating by -0.2% against

the Indian Rupee on the spot market. India 10Y G-Sec yields

fell by -0.2 bps, while US 10Y G-Sec yield rose by +23.9 bps,

and the German Bund yield rose by +26.6 bps, with rates

settling at 7.18%, 4.12% and 2.29% respectively. US yields

falling were a function of the expectations of the Fed’s

comments on potential rate cuts in 2024 with inflation

moderating sharper than expected.

Domestic Macro & Markets

The S&P BSE SENSEX (-0.7%) remained flat in January 2024. S&P

BSE Mid-cap and Small-cap indices outperformed the large cap

index, up +5.3% and 7.1% respectively. Sector-wise, Oil & Gas,

PSU, and Realty were the top 3 performers over the month,

clocking +12.6%, +11.2%, and +9.4%, respectively. 10 of S&P

BSE’s 13 sectoral indices ended the month in green.

Net Foreign Institutional Investors (FII) flows into equities

were negative for January 2024 (-$3.35 Bn in January 2024,

following +$5.85Bn in December). Domestic Institutional

Investors (DIIs) remained net buyers of Indian equities

(+$3.3Bn, from +$1.5Bn from last month).

India's high frequency data update:

Elevated levels of GST collections, festive season demand

uptick, stable retail inflation, deflated input inflation,

rising core sector outputs, and elevated credit growth augurs

well for the Indian economy.

Manufacturing PMI:

Manufacturing PMI in January 2024 recovered to 56.5, at a

four-month high and remained in expansion zone for the 31st

straight month driven by mild input cost inflation and surge

in new orders.

GST Collection:

Collections of INR 1.72 Tn (+10% YoY) in January 2024

concluded the twenty third consecutive month of collections

over the INR 1.4 Tn mark, following record collections of INR

1.87 Tn in April 2023. Collections for 8 out of 10 months in

this fiscal year crossed INR 1.6 Tn. Rising compliance,

increased formalization of the economy, festive demand, and

improved administrative efficiency have driven high tax

collection buoyancy.

Core sector production:

The index of eight core sector industries grew by 3.8% in

December 2023, against a 7.8% jump in November 2023, as an

unfavourable base effect came into play for India’s eight core

sectors. Seven of the eight constituent sectors recorded

positive YoY growths, with crude oil recording a YoY degrowth.

Industrial Production:

Manufacturing Output as measured by the IIP index decelerated

MoM to an eight-month low, with a rise of 2.4% in November

2023, vs a growth of 11.6% YoY in October, driven by muted,

but positive YoY growths in all 3 constituent sectors- Mining,

Manufacturing and Electricity.

Credit growth:

Scheduled Commercial Bank Credit growth reached 20.3% YoY as

of 12th January 2024 against a YoY growth of 16.47% as

observed on 13th January 2023.

Inflation:

December 2023 CPI inflation rate rose to a four-month high,

and reached 5.69%, accelerating from 5.55% in November 2023.

Food inflation remained elevated and accelerated, coming in at

9.53%. WPI inflation reached a nine-month high, with the

December print at +0.73%, 47 bps up from November’s at +0.26%,

as WPI inflation printed positive for the second month in a

row.

Trade Deficit:

Indian Merchandise Exports rose by +0.97% YoY to $38.45 Bn in

December 2023, while Imports fell by -4.85% YoY to $58.25 Bn.

Merchandise trade deficit narrowed to a $19.8 Bn as the global

economic situation remained uncertain.

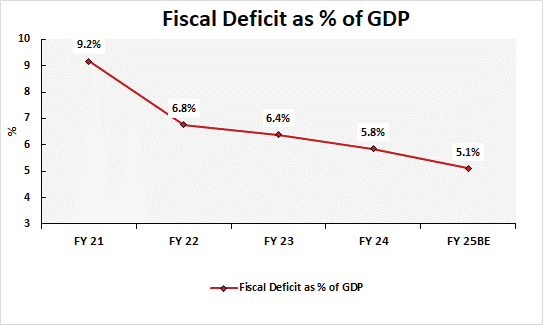

Interim Budget for Fiscal 2024-25 key takeaways:

A well-balanced budget with commitment to fiscal

consolidation, policy continuity and macro stability

Amidst various uncertainties the Central Government

continued the path of fiscal consolidation. FY25 deficit was

set at 5.1% of GDP signalling the intent to get to the

medium term fiscal deficit target of 4.5% of GDP in FY26.

Fiscal math appears credible with very reasonable

assumptions on tax and non-tax revenues growth for FY25.

On the expenditure side the focus has been on the supply

side. Effective capex allocation has been increased by

nearly 17%yoy while revenue expenditure is budgeted to see

very modest growth in FY25.

Events to watch out for in January 2024:

Oil Prices:

The OPEC+ rolled over its production cut policy for the first

quarter of 2024, with expectations of a revisit in March of

2024. Current production cuts remain at 2.2 Mn BPD (Barrels

per day), with Saudi Arabia maintaining a 1 Mn BPD voluntary

cut in production. Talks of impeding ceasefire between Hamas

and Israel, the situation in the Red Sea, unforeseen refinery

shutdowns in the USA, US rate cut expectations etc may lead to

higher volatility in global markets.

China Macroeconomic situation:

China’s manufacturing activity contracted for the fourth month

in a row in January 2024, with the government’s fiscal

stimulus measures providing little support for a deflationary

situation that has enveloped the economy. Major Chinese

developer Evergrande’s $330 Bn default has also created a drag

on the property market of the country, which accounts for a

much as 20% of real activity in the country, according to the

IMF. Risks of contagion through the high-risk shadow banking

system in China remains a key monitorable for global equity

markets.

Monthly Performance for Key Indices:

Source: Bloomberg

.*Calendar year returns.

Note: Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Note: Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Market View

India continues to be one of the fastest growing major economy

supported by demographic advantage, deregulation & policy

reforms, digitization and demand (aspirational spending).

Overall outlook towards domestic capital markets remains

optimistic, supported by resilient domestic demand and the

signs of bottoming of global & domestic monetary tightening

cycle.

Prudent interim budget with a focus on fiscal consolidation,

policy continuity can help reduce external risks and aid in

attracting global investors.

Going forward the sentiment appears to buoyant supported by

India’s relatively better macros, possibility of higher

foreign flows and the narrative around policy continuity in

the upcoming general elections.

From an equity market perspective, some of the positives

appear to be considered in valuations and therefore return

expectations from near term perspective should be moderate.

We believe Large Cap oriented strategies appear to be better

placed on a risk- reward basis while Asset allocation products

can help to manage the downside risks

Asset allocation in line with investment goals and risk

appetite is important for better risk – return optimization.

Herein asset allocation funds can help in lowering volatility

and provide better balance to the overall portfolio mix.

Chart of the month :

Central Government chooses fiscal prudence over populism.

The path to fiscal consolidation continued in the interim

budget announcement, with the fiscal deficit reaching 5.8% in

2024, and estimated to be 5.1% of GDP in FY25. The Central

government remains on the fiscal glide path of 4.5% by FY26.

Source:

Budget Documents, BE – Budgetary Estimates, NIMF Research,

CEIC

Disclaimer: The information herein above is

meant only for general reading purposes and the views being

expressed only constitute opinions and therefore cannot be

considered as guidelines, recommendations or as a professional

guide for the readers. The document has been prepared on the

basis of publicly available information, internally developed

data and other sources believed to be reliable. The sponsors,

the Investment Manager, the Trustee or any of their directors,

employees, Associates or representatives (‘entities & their

Associate”) do not assume any responsibility for, or warrant

the accuracy, completeness, adequacy and reliability of such

information. Recipients of this information are advised to

rely on their own analysis, interpretations & investigations.

Readers are also advised to seek independent professional

advice in order to arrive at an informed investment decision.

Entities & their associates including persons involved in the

preparation or issuance of this material, shall not be liable

in any way for any direct, indirect, special, incidental,

consequential, punitive or exemplary damages, including on

account of lost profits arising from the information contained

in this material. Recipient alone shall be fully responsible

for any decision taken on the basis of this document.

*The sectors mentioned are not a recommendation to buy/sell

in the said sectors. Details mentioned above are for

information purpose only.