Macro and

Equity Market

Outlook

Equity Market

Outlook

Global Macro & Markets – Dec 2022

Indian markets fell in December, in line with major global markets.

The Nifty Index corrected by 3.6% in December, after closing at an

all-time high in November. Major indices largely fell over the month,

except for Hang Seng (+6.4%). The S&P500 (-5.9%), the Euro 50

(-4.3%), the MSCI World (-4.3%) and the Nikkei (-6.7%) witnessed

declines in December. Additionally, the MSCI EM, NIFTY 50 India,

BOVESPA Brazil, and MOEX Russia all fell by -1.6%, -3.6%, -2.4%, and

-0.9% MoM, respectively. LME Metals Index witnessed a rise of 1.5%

MoM owing to a weaker dollar and tight supplies, although the

rapid spread of COVID infections in China remained a concern for

demand growth. WTI (West Texas Intermediate) fell by -0.4%, while

Brent crude rose by 0.6% MoM. The Dollar index fell for the second

consecutive month, down 2.3% in December. Additionally, the US$

rose by 1.6% over the month vis-à-vis the Rupee. US, India, and

Germany 10Y GSec rates rose by 27, 5 and 64 bps MoM and settled

at 3.9%, 7.3% and 2.6% respectively.

2022 Round Up

Indian markets outperformed global peers in CY2022. The MSCI

World and MSCI EM lost -19.5% and -22.4%, while the Nifty50 Index

was up 4.3% at the end of the year. The Dollar finished the year 11.3%

stronger than the Rupee, while the Dollar index rose 8.2% over the

year. Commodities remained mixed in their returns, with the

London Metal Exchange falling by -11.5%, while WTI and Brent rose by

6.7% and 10.5% respectively over the year. Yields on the Indian, USA

and German 10Y bonds rose by 146, 296, and 314 bps respectively in

2022, in line with global monetary tightening policies.

Domestic Macro & Markets - Dec 2022

SENSEX fell by -3.6% in December. Mid-cap and small-cap indices

outperformed the large-cap index and were down -2.5% and -2%

respectively. All sectoral indices closed negative, barring Metals

(+3%). IT (-6%), Auto (-4.8%), and Power (6.8%) indices were the top

losers. Market breadth of the Sensex 500 index deteriorated over

the month with 62.9% stocks advancing in the index on 2nd

January 2023. FPI were buyers in Indian equities, at US$236mn.

Domestic institutions turned buyers at US$1.9bn, primarily led by

domestic mutual fund activity (inflows of US$1.3bn).

India's high frequency data update:

Sustained high levels of GST collections, strengthening, but

moderating core, resilient manufacturing & agricultural sector

outputs, moderating inflation and healthy credit growth augured well

for the Indian economy in an otherwise tough global macro economy.

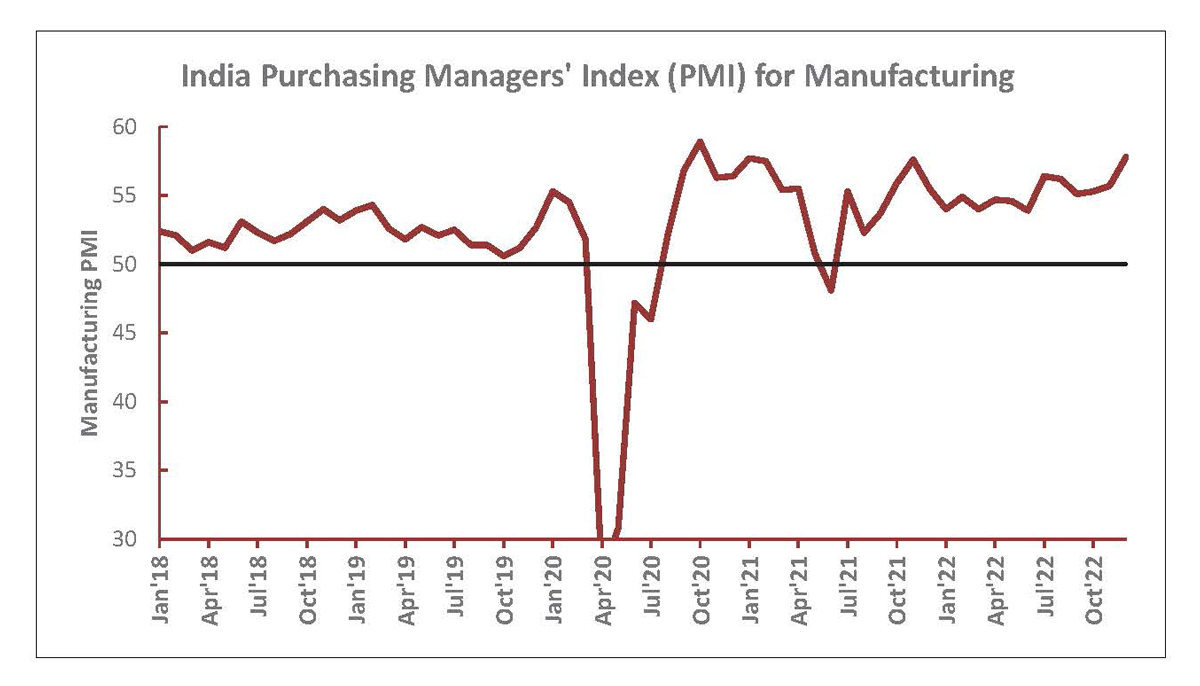

Manufacturing PMI:

Manufacturing PMI rose to a 26-month high in December 2022,

reaching 57.8, and remained in expansion zone (>50 points) for the

18th straight month, with a marked rise in new orders, near record

purchases of inputs, which stemmed from demand resilience, despite

the headwinds of slowing export and job creation growth rates.

GST Collection:

Collections of INR 1.49 Tn (+15% YoY, +2.5% MoM) in December 2022

concluded the tenth consecutive month of collections over the

1.4Tn mark, reflecting healthy festive activity and a steady

economic revival. The third highest collection this fiscal was in line

with the fiscal average, against the INR 1.23Tn in FY22. Increased

revenue from imports and domestic transactions have led to the

sustained collection levels.

Core sector production:

Core sector production growth rose MoM to 5.4% YoY in November

2022, owing to a healthy expansion in cement, steel, and coal.

Crude oil, petroleum refinery products and natural gas production

(which shrank for a fifth successive month) showed a decline

among the core sectors.

Industrial Production:

factory output as measured by the IIP index slumped to a

26-month low of -4% in October 2022 vs a rise of 3.1% YoY in

September 2022, after a contraction in capital goods output and

consumer goods (durables and non-durables) was seen.

Manufacturing declined after the combined headwinds of faltering

export performance and the struggling SME sector denting output.

Credit growth:

Credit growth accelerated to 17.44% YoY as of 16th December 2022

against YoY growth of 6.21% as observed on 17th December 2021.

Inflation:

November 2022 CPI inflation sank to a 11-month low of 5.88% from

6.77% in October 2022, led by easing food prices. WPI inflation

continued to drop sharply, with the November 2022 print at a

21-month low of 5.85%, 254 bps down from October 2022’s at 8.39%.

Trade Deficit:

Indian Merchandise Exports recorded a flat growth of 0.59% MoM to

$31.99 Bn in November 2022, while Imports rose by 5.37% to $55.88

Bn. India’s trade deficit narrowed MoM to $23.89 Bn from $26.89 Bn

in October 2022.

Govt savings rate rise:

The interest rate hike announced for small savings schemes

including post office term deposits, NSC, and senior citizen savings

scheme will be effective from 1st January 2023. Within the scheme,

the Government announce a rate hike that raised the interest rates

by 110 bps across the board of its small savings scheme. Interest

rates on Public Provident Fund (PPF) and the girl child savings

scheme Sukanya Samriddhi remains unchanged. The consecutive

quarterly rate hike comes after the rates were nearly unchanged

for 2 years. Rate changes in the scheme includes: 1) National

Savings Certificate (NSC) will yield a 7% interest rate from January 1

compared to 6.8% at present. 2) The one-year deposit will give 6.6%

interest against 5.5% currently, while two-year deposit will give 6.8%

interest against 5.7% currently. The three-year time deposit will give

6.9% interest against 5.8% currently, while 5-year time deposit will

give 7% interest against 6.9%. 3) Interest on senior citizen plans has

been raised to 8% from 7.6%.

Free Food Scheme extended by the Central Government:

The Cabinet approved the one-year extension of the free food

programme, with an INR 2 Tn subsidy burden that will be borne by

the government. In the announcement, the government merged

The Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) and the

National Food Security Act (NFSA) and notified the integrated

roll-out of the scheme would start from January 1st and last till

December 31st, 2023. Through the scheme, the government will

provide free food grains to 81.35 Crore beneficiaries of the NFSA

through its network of 5.33 Lakh fair price shops in the country.

Market View

As we enter 2023, we see an environment where both inflation and

growth might be slowing. Both from cyclical and structural

perspective, India seems to be better placed vs rest of the World.

Domestic demand continues to be strong. Policy reforms, huge

under investments in Capex, stronger corporate Balance Sheets

have potentially created a robust platform for a virtuous cycle of

growth.

While India is likely to be amongst the fastest growing economies,

the near-term global uncertainties are unlikely to wither away soon

and the volatility can be potentially higher in the short run.

We are attempting to maintain balanced portfolios through a

combination of domestic recovery themes along with secular

businesses. The attempt is to identify relatively better valued

opportunities across these themes.

From an investor’s perspective given the external risks and its

potential impact investing in a staggered manner or systematic

route may help iron out market extremes. Given our view that

broader markets may do well with the present fundamentals,

long-term investors can consider diversified strategies like

multi-cap or flexi-cap offerings for equity investments.

Conservative investors seeking equity exposure with lower volatility

may consider asset allocation strategies like - Balanced

Advantage/Asset Allocator which manage equity allocations

dynamically.

Note:The sectors mentioned are not a recommendation to buy/sell in the said sectors.

The schemes may or may not have future

position in the said sectors. For complete details on Holdings & Sectors of NIMF schemes, please visit

website mf.nipponindiaim.com.

Past performance may or may not be sustained in future

Past performance may or may not be sustained in future

Chart of the month :

India's manufacturing sector performance remains resilient. The

gap between India’s manufacturing PMI reading versus the rest of

the World remains elevated.

Common Source:

CMIE, Nippon India Mutual Fund Research, Bloomberg

Disclaimer:The information herein above is meant only for general reading purposes and

the views being expressed only

constitute opinions and therefore cannot be considered as guidelines, recommendations or as a

professional guide for

the readers. The document has been prepared on the basis of publicly available information, internally

developed data

and other sources believed to be reliable. The sponsors, the Investment Manager, the Trustee or any of

their directors,

employees, Associates or representatives (‘entities & their Associate”) do not assume any responsibility

for, or warrant the

accuracy, completeness, adequacy and reliability of such information. Recipients of this information are

advised to rely on

their own analysis, interpretations & investigations. Readers are also advised to seek independent

professional advice in

order to arrive at an informed investment decision. Entities & their associates including persons

involved in the preparation

or issuance of this material, shall not be liable in any way for any direct, indirect, special,

incidental, consequential, punitive

or exemplary damages, including on account of lost profits arising from the information contained in

this material.

Recipient alone shall be fully responsible for any decision taken on the basis of this document.