Macro and

Equity Market

Outlook

Equity Market

Outlook

GLOBAL MACRO & MARKETS

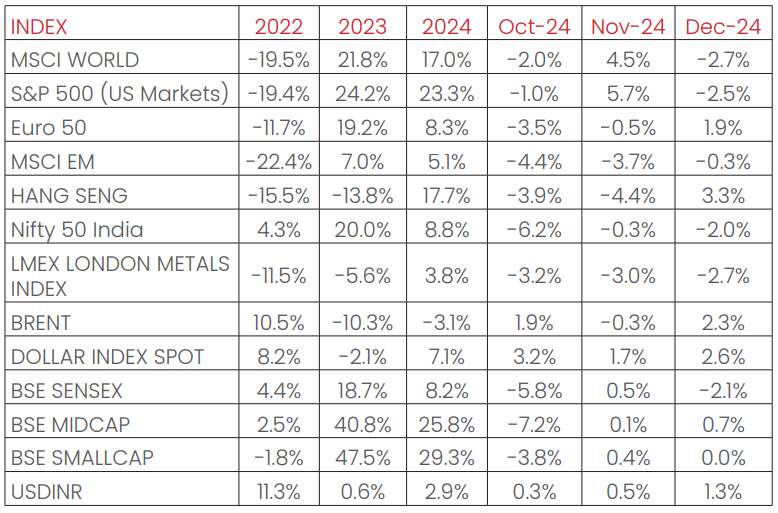

India’s NSE NIFTY index ended the month of December 2024

negative (-2.0%). Among major global indices, the S&P500 (-2.5%),

The Morgan Stanley Capital International (MSCI) World (+4.5%), the

Euro 50 (-1.9%), and the Japanese NIKKEI (+4.4%) ended the month,

December 2024 with mixed returns. Performance was mixed

among Emerging Markets (EM) indices as well, with the Morgan

Stanley Capital International Emerging Markets (MSCI EM), the

Hang Seng (Hong Kong), the BOVESPA Brazil (BVSP) recording

sequential returns of (-0.3%), (+3.3%), and (-4.3%) respectively.

The London Metals Exchange (LME) Metals Index fell by (-2.7%) in

December 2024, driven by weak global demand and limited

economic recovery in largest consumer market, in China. The West

Texas Intermediate (WTI) and Brent Crude rose MoM, by (+5.5%)

and (+2.3%), respectively, as markets rallied despite stronger dollar,

Non- Organization of the Petroleum Exporting Countries (OPEC)

supplies rose to offset on strong demand.

The Dollar index appreciated by (+2.6%) through December 2024,

with the US Dollar (USD) losing vis-à-vis Emerging Market (EM)

currencies (-2.1%) and appreciating against the Indian Rupee (INR)

(+1.3%). India 10Y G-Sec yields rose by (+2 bps), while US 10Y G-Sec

yields rose by (+40 bps), and the German Bund yield fell by (-28

bps), with rates settling at 6.76%, 4.56% and 2.36% respectively.

Domestic Macro & Markets

The BSE SENSEX (-2.1%) fell in December 2024, in line to the NSE NIFTY

index. The BSE Mid-cap index and the BSE Small-Cap index

outperformed the BSE SENSEX, rising by (+0.8%), and 0.0% over the

month, December 2024 respectively. Sector-wise, Healthcare,

Realty and Consumer Durables were the top 3 performers over the

month, December 2024 clocking (+3.7%), (+3.4%), and (+3.1%),

respectively. 4 of BSE’s 13 major sectoral indices ended the month,

December 2024 in green.

Net Foreign Institutional Investors (FII) flows into equities turned

positive for December 2024 (+$ 1.3 Bn, following $ -2.7 Bn in

November 2024). The Domestic Institutional Investors (DIIs)

remained net buyers of Indian equities for the 17th month in

December 2024 (+$4.0 Bn, from +$5.3 Bn last month, November

2024). In Calendar Year (CY2024), Net Foreign Institutional Flows

(FII) Flows stood at (-$0.12 Bn), while net Domestic Institutional

Investors (DII) investments in the cash markets stood at (+$62.9

Bn), outpacing the Foreign Institutional Investors (FII) investments.

India's high frequency data update:

Record levels of Goods and Services Tax (GST) collections, stable retail

inflation, deflated input inflation, rising core sector outputs, and

elevated credit growth augurs well for the Indian economy.

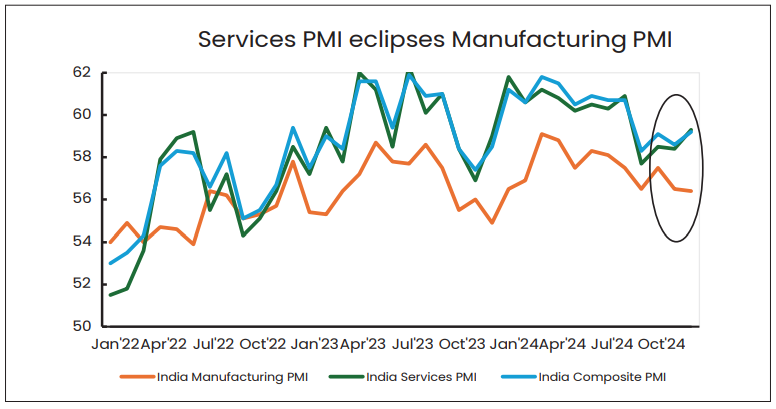

Purchasing Managers’ Index Manufacturing PMI:

India’s Manufacturing Purchasing Managers’ (PMI) in December 2024

slowed month on month to 56.4 (vs 56.5 in November 2024),

remaining in expansion zone (>50) for the 41st straight month. The

slowdown was a result of slowing new orders, but manufacturing

performance remained comfortably in the expansion zone.

Goods and Services Tax (GST) Collection:

Gross collections of INR 1.77 Tn (+7.2% YoY) in December 2024

concluded the thirty fourth consecutive month of collections over

the INR 1.4 Tn mark, following previous record collections of INR 2.1 Tn

in April 2024. Rising compliance, higher output prices, festive

season demand, rising collections from imports and domestic

transaction volume uptick has driven elevated tax collections.

Core Sector Production:

The index of eight core sector industries grew to a four-month high

by (+4.3%) YoY in November 2024, against a (+3.1%) growth in

October 2024, as an unfavourable base effect came into play. Six

out of eight constituent segments grew YoY, driven by Cement

production (+13% YoY).

Industrial Production:

Factory output growth as measured by the Index of Industrial

Production (IIP) accelerated MoM to (+3.5%) in October 2024, vs a

growth of (+3.1%) YoY in September 2024, driven by positive, and

YoY growths in 3 of 3 major sectors- Manufacturing, Mining,

Electricity.

Credit growth:

Scheduled Commercial Bank Credit growth reached (+11.15%) YoY

as of 15th November 2024 against a YoY growth of (+20.64%) as

observed on 17th November 2023, as a strong base effect came to

play post the merger of Housing Development Finance

Corporation (HDFC and HDFC Bank).

Inflation:

November 2024 Consumer Price Index (CPI) inflation rate

decelerated MoM to (+5.48%), down from 6.21% in October 2024.

Food inflation came in at a slower pace, at (-8.2%). The Wholesale

Price Index (WPI) inflation decelerated sequentially in November

2024, with the print at (+1.89%), 47 bps down from October 2024.

Trade Deficit:

Indian Merchandise Exports fell by (+4.86%) YoY to $32.1 Bn in

November 2024, while Imports rose by (+27%) YoY to $69.95 Bn.

Merchandise trade deficit widened by (77%) YoY to $37.84 Bn.

Events to watch out for in January 2025:

The Reserve Bank of India (RBI) Policy Stance:

After keeping the policy repo rate unchanged at 6.5% in December

2024, The RBI remains cautious, having changed the policy stance

to “neutral” in the October 2024 meet. Expectations for a change in

the rate will remain data driven, particularly inflation.

The Federal Open Market Committee (FOMC) Meeting:

The Federal Open Market Committee (FOMC) meets on January

29th ,2025 to discuss further rate cuts, after cutting rates by 100 bps

in the last 3 meetings in September 2024, November 2024 and

December 2024. The policy rate stands at 4.25%-4.5%, and

expectations of a slower rate cut in January 2025 are priced in by

the markets. Data flow, especially labour market and inflation may

drive further changes in policy rates.

Other things to watch out for:

China Stimulus, India and US earnings Seasons and Oil Market

volatility remain key events for markets to watch out for.

Monthly Performance for Key Indices:

Source: Bloomberg

.*Calendar year returns.

Note:Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Note:Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Market View

In December 2024, Indian equity markets ended on a spectacular

note for the 9th straight year in a row in CY’24, shrugging off

several uncertainties both global & local.

Key Factors that influenced the Indian markets’ move in CY’24

include: Change in the political landscape, Geopolitical unrest,

Stimulus by China, Lower earnings by Indian companies and

divergent moves by Global Central Banks.

On the domestic front, weaker near-term growth trends, weak

corporate earnings, elevated valuations, Foreign Portfolio

Investment (FPI) outflows led to sharp fall in recent 2-3 months.

Mid-Small cap segments outperformed the large caps supported

by sustained flows from domestic investors, while Foreign Portfolio

Investment (FPI) outflows was more pronounced in the larger

businesses. Midcap valuations are currently, expensive compared

with Large cap and small cap due to sudden surge in the last ten

months. Large cap valuations are hovering near their 3-year avg

level since Jan 2024, while midcap and small cap are well above

their 3 year average level.

Post the recent corrections overall valuations appear to be

moderating in relative terms. Given the anticipated demand pick

up we expect the muted earnings growth of last 2 quarters to

improve. Some of the potential triggers for demand revival may

include - Rural Agricultural recovery (Rabbi crops), extended

wedding/festive season, higher Government spending and

moderating inflation.

The new Policy actions in the United States (US) post new

government may lay the trend towards global growth shift in the

next 1-2 years

Investors are likely to take cues from global trade & monetary

policies especially the United States (US). From a domestic

perspective corporate earnings maybe a key market trigger.

Accordingly, investors can consider well diversified large

cap-oriented strategies like Large/Flexi/Multi Cap appear over the

medium term to manage the likely near term uncertainties .

Investors seeking better downside protection may consider asset

allocation products like Multi Asset Allocation, Dynamic Equity, etc

across Hybrid space.

Long term investors with appropriate risk appetite can consider

Mid and Small Cap allocations in staggered manner through the

systematic route.

Chart of the Month:

Weak 2Q GDP show raises policy support expectations

The S&P India Services Purchasing Managers’ Index (PMI) for

December 2024 rose to a four month high of 59.3 points, an

increase from 58.4 points recorded in November 2024. The HSBC

(Hong Kong and Shanghai Banking Corporation) India

manufacturing Purchasing Managers’ Index (PMI) for December

2024 slipped to a 12-month low at 56.4. The divergence suggests

optimism of services companies in new business and future

activities, even as production and fresh orders for manufacturers

slowed down. With both in expansion territory (>50), economic

activity momentum is expected to continue, albeit with services

leading performance on the back of an improved outlook for fresh

orders.

Source:

NIMF Research, Bloomberg

Disclaimer:

The information herein above is meant only for general reading purposes and the views being expressed

only constitute

opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide

for the readers.

The document has been prepared on the basis of publicly available information, internally developed

data and other

sources believed to be reliable. The sponsors, the Investment Manager, the Trustee or any of their

directors, employees,

Associates or representatives (‘entities & their Associate”) do not assume any responsibility for, or

warrant the accuracy,

completeness, adequacy and reliability of such information. Recipients of this information are advised

to rely on their own

analysis, interpretations & investigations. Readers are also advised to seek independent professional

advice in order to

arrive at an informed investment decision. Entities & their associates including persons involved in

the preparation or

issuance of this material, shall not be liable in any way for any direct, indirect, special,

incidental, consequential, punitive,

or exemplary damages, including on account of lost profits arising from the information contained in

this material.

Recipient alone shall be fully responsible for any decision taken on the basis of this document.

The sectors mentioned are not a recommendation to buy/sell in the said sectors. Details mentioned

above are for

information purpose only.