Macro and

Equity Market

Outlook

Equity Market

Outlook

GLOBAL MACRO & MARKETS

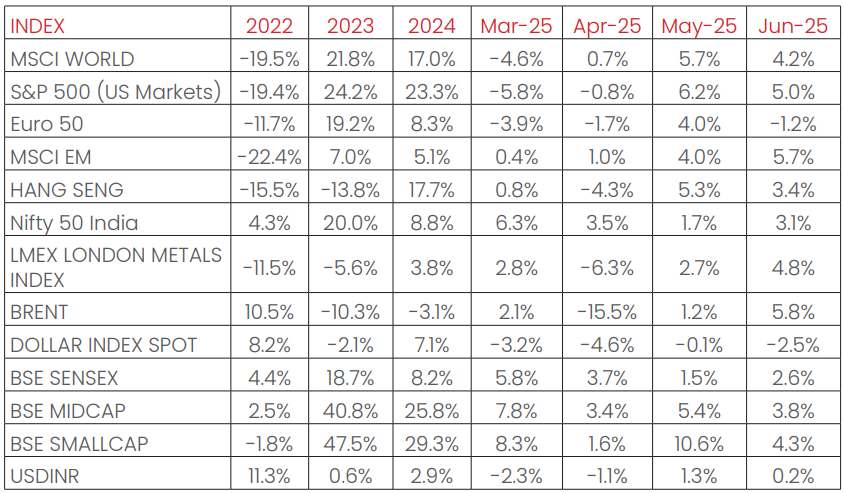

India’s NSE NIFTY index ended the month of June 2025 in green

(+3.1%). Among major global indices, the S&P500 (+4.6%), the

Morgan Stanley Capital International (MSCI) World (+4.3%), the

Japanese NIKKEI (+6.6%) ended the month of June 2025 with

positive returns while the Euro 50 (-0.98%) ended the month of

June 2025 in the red. Performance was positive among Emerging

Market (EM) indices as well, with the Morgan Stanley Capital

International Emerging Markets (MSCI EM), Hang Seng (Hong Kong),

BOVESPA Brazil (BVSP) recording sequential returns of (+5.7%),

(+3.4%), and (+1.3%) respectively.

The London Metals Exchange (LME) Metals Index rose (+4.8%) in

June 2025, as global trade tensions remained heightened. West

Texas Intermediate (WTI) and Brent Crude rose MoM, by (+7.1%) and

(+5.8%), respectively, as markets remained cautious given tariff

fears and geopolitical tensions in the Middle East.

The Dollar index declined (-2.5%), through June 2025, with the US

Dollar (USD) appreciating vis-à-vis Emerging Market (EM)

currencies (+1.7%) and appreciation against the Indian Rupee (INR)

on the spot market (+0.2%). India 10Y G-Sec yields rose by 3.6 bps,

while US 10Y G-Sec yields fell by 17.2 bps, and the German Bund yield

rose by 10.7 bps, with rates settling at 6.32%, 4.28% and 2.60%,

respectively.

Domestic Macro & Markets

The BSE SENSEX (+2.6%) rose in June 2025, in line with the NSE NIFTY

Index. The BSE Mid-cap index and the BSE Small-Cap index

outperformed the BSE SENSEX, rising by (+3.8%), and (+4.3%) over

the month of June 2025, respectively. Sector-wise, Teck, Healthcare

and Realty were the top outperformers over the month of June

2025, clocking (+4.7%), (+3.9%), and (+3.8%), respectively. Except

FMCG, all of BSE’s 12 remaining major sectoral indices ended the

month of June 2025 in green.

Net Foreign Institutional Investors (FII) flows into equities were

positive for June 2025 (at +$1.69 Bn, following +$1.57 Bn in May 2025).

Domestic Institutional Investors (DIIs) remained net buyers of

Indian equities for the 22nd consecutive month (+$8.46 Bn, from

+$7.92 Bn last month, May 2025).

India's high frequency data update:

Record levels of Goods and Services (GST) collections, stable retail

inflation, deflated input inflation, rising core sector outputs, and

elevated credit growth augurs well for the Indian economy.

Purchasing Managers’ Index Manufacturing PMI:

Manufacturing (PMI) in June 2025 rose to a fourteen-month high of

58.4 (vs 57.6 in May 2025), remaining in expansion zone (>50) for the

46th straight month. Driven by new export orders that saw their third

highest growth rate since 2005. Intermediate goods producers led

growth in terms of volume, while the consumer and capital goods

sectors saw moderate growth.

Goods and Services Tax (GST) Collection:

Gross collections of INR 1.84 Tn (+6.2% YoY) in June 2025 concluded

the thirty ninth consecutive month of collections over the INR 1.4 Tn

mark, following previous record collections of INR 2.1 Tn in April 2024.

Rising compliance, higher output prices, rising collections from

imports and domestic transaction volume uptick has driven

elevated tax collections.

Core Sector Production:

The index of eight core sector industries grew by 0.7% YoY in May

2025, against a 0.5% growth in April 2025. Four out of eight

constituent segments grew YoY, driven by Cement (9.2% YoY) and

Steel production (6.7% YoY).

Industrial Production:

Factory output growth as measured by the Index of Industrial

Production (IIP) decelerated MoM to +1.2% in May 2025, vs a growth

of +2.7% YoY in April 2025, driven by growth in manufacturing sector

at 2.6%.

Credit growth:

Scheduled Commercial Bank Credit growth slowed to 9.8% YoY as

of 30th May 2025 against a YoY growth of 16.2% as observed in May

2024, as sector-wise credit in May 2025 slowed down in all sectors.

Agriculture and allied activities credit rose by 7.5 %, lower than 21.6

% a year ago, while industrial sector credit grew by 4.9 per cent,

down from 8.9 % in May 2024.

Inflation:

May’s Consumer Price Index (CPI) inflation rate decelerated MoM to

2.82%, down from 3.16% in April 2025, recording the Lowest YoY

inflation since February 2019. Food inflation came in at a slower

pace MoM, at 0.99%, down from 1.78% in the previous month of April

2025, which is the lowest it has been since October 2021. The

Wholesale Price Index (WPI) inflation rose sequentially, albeit

slower, in May 2025, with the print at 0.39%, 46 bps up from April

2025.

Trade Deficit:

India's merchandise imports were down 1.7% YoY to $60.61 billion in

May 2025, while exports for the month of May 2025 were down 2.77%

YoY to $38.73 billion, resulting in a contraction of the merchandise

trade deficit to $21.88 billion by 0.95% YoY.

Events to watch out for in July 2025:

Trade Related News flow:

Tariff news flow remains volatile with

90-day deadlines upcoming in July 2025. Tariffs will be monitored

closely by the markets. Indian bilateral trade agreements to be

watched.

The Reserve Bank of India’s Monetary Policy Committee (RBI

MPC) Meet:

The MPC will be meeting starting 4th August, 2025 in

what will be the third MPC meet of FY26 and will announce its

decision regarding the benchmark rates on 7th August 2025. In the

Meet held from 4th-6th June, 2025, RBI cut repo rate by 50bps

bringing it down to 5.50%, CRR was also cut by 100bps in an attempt

to improve liquidity in the system. RBI will intend to help boost

India’s single digit credit growth environment.

Federal Open Market Committee (FOMC) Meet:

The Federal Open

Market Committee’s (FOMC) last meet was held on June 16th–18th,

2025 where the Fed Funds Rate were kept unchanged at 4.25% to

4.5%. The minutes of this meeting showed internal concern over the

effects of the Trade policy. Officials said they saw a risk of

persistent inflation, a weakening labour market, and slowing

economic growth. The next FOMC meeting will be held on July

29th–30th, 2025. Economic high frequency data will be a key

monitorable going into the FOMC’s meet.

Other things to watch out for:

Oil Market volatility with the

Organization of the Petroleum Exporting Countries (OPEC+)

increasing production, and Monsoon related news remain key

events for markets to watch out for.

Monthly Performance for Key Indices:

Source:NIMF Research, Bloomberg

.*Calendar year returns.

Note:Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation

Past performance may or may not be sustained in future.

Note:Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation

Past performance may or may not be sustained in future.

Market View

Equity markets registered gains even as the uncertainties from

global policies, geopolitical tensions continued. Investors

worldwide appeared hopeful that the Tariff challenges may be

addressed with lower economic impact.

Lower inflation and benign interest rate policy are likely to support

domestic economic recovery. Above- average rainfall is driving

optimism in rural focused sectors. Lower interest rates

environment coupled with some tax relief on consumption may

help consumer discretionary segments to perform better in the

coming quarters.

Lower inflation and benign interest rate policy are likely to support

domestic economic recovery. Above- average rainfall is driving

optimism in rural focused sectors. Lower interest rates

environment coupled with some tax relief on consumption may

help consumer discretionary segments to perform better in the

coming quarters.

Increased geopolitical developments has kept markets volatile

post recovery from lows. Despite stabilizing global macros, risks

remain, geopolitical tensions, policy shifts and overall weak

external demand.

Valuations have again firmed up for the broader market after

recent rally. Scope for rerating seems limited hereon and therefore

market may track earnings trajectory for further gains.

Domestic market resilience can be attributed to the underlying

domestic growth dynamics and estimated lower direct impact of

tariffs.

Large Cap & Large Cap oriented strategies along with hybrid funds

appear better placed on risk-reward basis, while Mid/Small cap

allocation may be considered in a staggered manner through

systematic investment with a long-term view.

Overall, we believe while the market may be impacted by macro

developments /events in the near term the medium-term outlook

remains optimistic on supportive domestic fundamentals

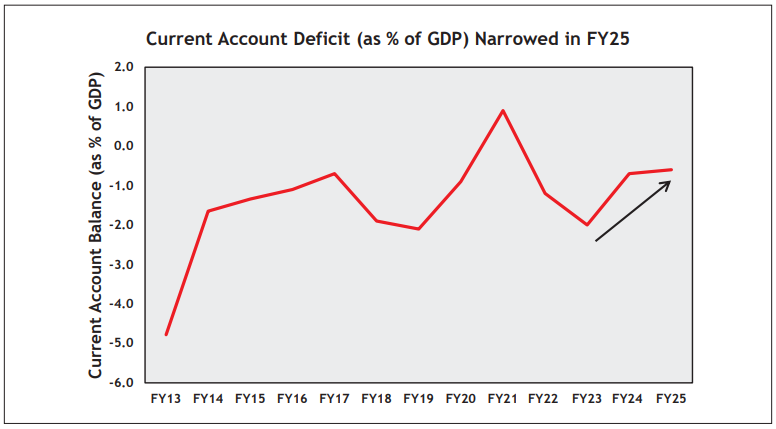

Chart of the Month:

India’s current account balance posted a surplus of $13.5 billion, or

1.3% of Gross Domestic Product (GDP), during Q4-FY25. This surplus

comes after a gap of three quarters of deficit, reflecting the

contribution of a surge in services exports.

For FY25, Current Account Deficit (CAD) moderated to $23.3 billion

(0.6% of GDP) from $26 billion (0.7% of GDP) in FY24. This was on the

back of a higher net invisible receipts.

Source:

RBI, NIMF Research

Note:

All data as on 30th June 2025 unless mentioned otherwise

Disclaimer:

The current fund philosophy may change in future depending on market conditions or fund manager’s

views. The

sectors mentioned are not a recommendation to buy/sell in the said sectors. The scheme may or may not

have future

position in the said sectors.

The information herein above is meant only for general reading purposes and the views being expressed

only constitute

opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide

for the

readers. The document has been prepared on the basis of publicly available information, internally

developed data and

other sources believed to be reliable. The sponsors, the Investment Manager, the Trustee or any of

their directors,

employees, Associates or representatives (‘entities & their Associate”) do not assume any

responsibility for, or warrant

the accuracy, completeness, adequacy and reliability of such information. Recipients of this

information are advised to

rely on their own analysis, interpretations & investigations. Readers are also advised to seek

independent professional

advice in order to arrive at an informed investment decision. Entities & the associates including

persons involved in the

preparation or issuance of this material, shall not be liable in any way for any direct, indirect,

special, incidental,

consequential, punitive, or exemplary damages, including on account of lost profits arising from the

information

contained in this material. Recipient alone shall be fully responsible for any decision taken on the

basis of this document