Macro and

Equity Market

Outlook

Equity Market

Outlook

GLOBAL MACRO & MARKETS

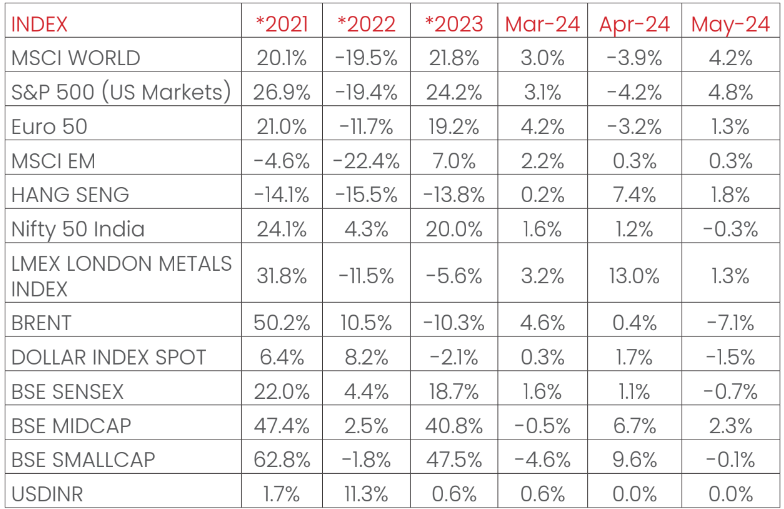

India’s NSE NIFTY index ended the month marginally down,

(-0.3%) MoM, in May 2024. The S&P500 (+4.8%), the Euro 50

(+1.3%), the Morgan Stanley Capital International (MSCI) World

(+4.2%), and the Japanese NIKKEI (+0.2%) all ended the month,

May 2024 in positive. Performance was mixed among Emerging

Market (EM) indices, with the Morgan Stanley Capital

International (MSCI) Emerging Markets (EM) and the HANG SENG

(Hong Kong), ending the month, May 2024 in green, with returns

of +0.3% and +1.8%, respectively. The BOVESPA (BVSP) Brazil

and the MOEX RUSSIA index ended the month, May 2024 in

negative, with returns of (-3.0%) and (-7.3%) respectively.

The London Metals Exchange (LME) Metals Index rose (+1.3%) in

May 2024, as base metals demand outpaced tighter supplies, and

manufacturing data from China, the largest consumer, grew at a

faster pace

The West Texas Intermediate (WTI) and Brent Crude fell MoM, by

(-6.0%) and (-7.1%) respectively even as oil cuts by The

Organization of the Petroleum Exporting Countries (OPEC+) may

extend into the year 2025.

The Dollar index depreciated by (-1.5%) through May 2024, with

the Dollar appreciating by +1.1% vis-à-vis Emerging Market

(EM) currencies and remaining flat against the Indian Rupee

(INR) on the spot market. India 10Y G-Sec yields fell by 21

bps, while US 10Y G-Sec yield fell by 18 bps, and the German

Bund yield rose by 8 bps, with rates settling at 6.97%, 4.50%

and 2.66% respectively.

Domestic Macro & Markets

The S&P BSE SENSEX (-0.7%) remained flat in May 2024, in line

with the NSE NIFTY index. BSE Mid-cap and Small-cap indices

outperformed the S&P BSE Sensex, with performances of +2.3%

and (-0.1%) respectively. Sector-wise, Capital Goods, Power,

and Metals were the top 3 performers over the month, May 2024,

clocking +11.2%, +6.6%, and +4.7%, respectively. 6 of S&P

BSE’s 13 sectoral indices ended the month May 2024 in green.

Net Foreign Institutional Investors (FII) flows into equities

were negative for May 2024 (-$ 3.15 Bn (Up to May 29th, 2024,

following (-$ 1.3) Bn in April 2024). The Domestic

Institutional Investors (DIIs) remained net buyers of Indian

equities (+$6.43 Bn (Up to May 30th, 2024), from +$5.30 Bn

last month). In CYTD2024, Net Foreign Institutional Investors

(FII) Flows stood at -$2.8 Bn, while net Domestic

Institutional Investors (DII) investments in the cash markets

stood at +$19.17 Bn, outpacing Foreign Institutional Investors

(FII) investments.

India's high frequency data update:

Record levels of Goods and Services Tax (GST) collections,

stable retail inflation, deflated input inflation, rising core

sector outputs, and elevated credit growth augurs well for the

Indian economy.

Manufacturing PMI:

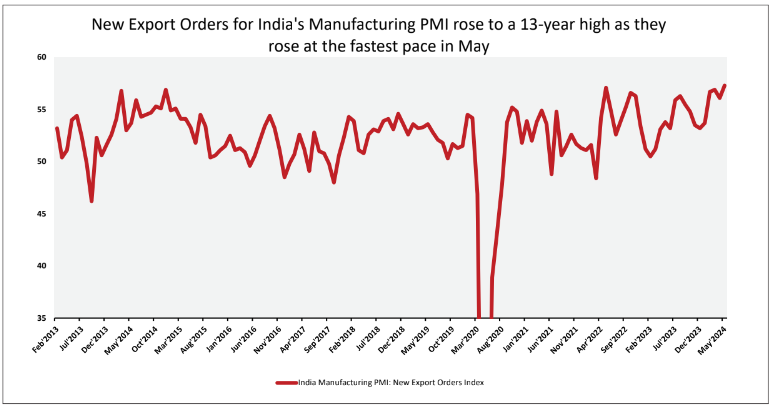

India’s Manufacturing Purchasing Managers' Index (PMI) in May

2024 remained strong at 57.5 (vs 58.8 in April 2024),

remaining in expansion zone for the 34th straight month driven

by accelerating new export orders and jobs growth.

GST Collection:

Gross collections of INR 1.73 Tn (+10% YoY) in May 2024

concluded the twenty seventh (27th) consecutive month of

collections over the INR 1.4 Tn mark, following previous

record collections of INR 2.1 Tn in April 2024. Rising

compliance, increased formalization of the economy, and

domestic transaction volume uptick has driven elevated tax

collections.

Core sector production:

The index of eight core sector industries accelerated YoY to

+6.2% in April 2024, against a +6% jump in March 2024 (Revised

upwards from +5.2%). On a sequential basis, however, the index

fell by (-8.1%), the sharpest pace in last 12 months.

Typically, April 2024 witnesses a contraction in production as

compared to March 2024.

Industrial Production:

Factory output growth as measured by the Index of Industrial

Production (IIP) decelerated to (-4.9%) in March 2024, vs a

growth of +5.7% YoY in February 2024, driven by positive YoY

growths in 3 major sectors- Mining, Manufacturing and

Electricity.

Credit growth:

Scheduled Commercial Bank Credit growth reached 19.54% YoY as

of 17th May 2024 against a YoY growth of 15.42% as observed on

19th May 2023.

Inflation:

April’s 2024 Consumer Price Index (CPI) inflation rate reached

a 11-month low of 4.83%, decelerating from 4.85% in March

2024. Food inflation decelerated, coming in at 7.87%.

Wholesale Price Index (WPI) inflation accelerated from March

2024, with the April 2024 print at +1.26%, 73 bps up from

March 2024, as WPI inflation printed positive for the sixth

month in a row.

Trade Deficit:

Indian Merchandise Exports rose by +1.07% YoY to $34.99 Bn in

April 2024, while Imports rose by +10.26% YoY to $54.09 Bn.

Merchandise trade deficit widened by +32.29% YoY to $19.1 Bn

as oil exports grew YoY.

Events to watch out for in June 2024

The Federal Open Market Committee (FOMC) meet:

The Federal Reserve meets on June 11th-12th 2024, with rate

cuts unlikely. A year since the Federal Funds rate were last

raised to 5.25%-5.5% in July 2023, the fed maintains a

“robust”, with a keen eye on inflation and job market numbers.

Economic activity in the USA may continue to expand, and rate

cut decisions will be data driven.

Heat/ Monsoon:

India Meteorological Department (IMD) retained its long-range

south-west monsoon forecast at above normal long period

average (LPA) in its second forecast release. The forecast of

above-normal rainfall augurs well for kharif sowing this year,

though the distribution of rainfall across different regions

and states will play a crucial role in determining the quantum

of food grain production. As of 24 May 2024, overall water

levels in reservoirs are 5% below normal, which deviates from

the 10-year average.

Central Government Formation and Budget:

Key catalysts for the market will be among others, the cabinet

formation post-election, first 100 days agenda/major policy

announcements, and the FY24-25 full year budget in July 2024.

Ministry allocations, policy trajectory and budget priorities

remain a key monitorable for the market over June 2024.

Monthly Performance for Key Indices:

Source: Bloomberg

.*Calendar year returns.

Note: Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Note: Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Market View

The biggest takeaway of the general election outcome is the

likely policy continuity across key facets like development

and reforms. This along with India’s strong fundamentals,

domestic demand resilience, and policy support may help

provide buffers against external shocks.

Hence, we maintain our optimistic view in terms of economic

growth as reforms of the past are enough to support future

growth.

Investment cycle is expected to continue with greater

participation from private sector, assuming no major shifts in

the global dynamics and risk appetite.

Consumption especially the rural part appears well placed for

a recovery supported by low base, falling inflation and

expectations of above normal monsoons.

Post the election results we can expect sector rotation based

on valuations and relative growth prospects.

We believe mid-teen earnings improvement is possible at a

broad level. Going forward its estimated that market

performance may be largely dependent on earnings growth.

In our view Large Cap oriented strategies like

Large/Flexi/Multi Cap appear better placed while on the

thematic space Banking & Financial services space appears

interesting on relative valuations.

In line with the medium term perspective Mid and Small Cap

allocations in staggered manner through the systematic route

Chart of the month :

Indian exports have been under pressure in the last few quarters. There are now signs of recovery in exports. For instance, new export orders within India Purchasing Managers’ Index (PMI) manufacturing survey rose to a 13-year high of 57.3 in May 2024 (vs. 56.1 in April 2024), as firms reported gains from clients across most regions.

Source:

NIMF Research, CEIC

Disclaimer: The information herein above is

meant only for general reading purposes and the views being

expressed only constitute opinions and therefore cannot be

considered as guidelines, recommendations or as a professional

guide for the readers. The document has been prepared on the

basis of publicly available information, internally developed

data and other sources believed to be reliable. The sponsors,

the Investment Manager, the Trustee or any of their directors,

employees, Associates or representatives (‘entities & their

Associate”) do not assume any responsibility for, or warrant

the accuracy, completeness, adequacy and reliability of such

information. Recipients of this information are advised to

rely on their own analysis, interpretations & investigations.

Readers are also advised to seek independent professional

advice in order to arrive at an informed investment decision.

Entities & their associates including persons involved in the

preparation or issuance of this material, shall not be liable

in any way for any direct, indirect, special, incidental,

consequential, punitive, or exemplary damages, including on

account of lost profits arising from the information contained

in this material. Recipient alone shall be fully responsible

for any decision taken on the basis of this document.

*The sectors mentioned are not a recommendation to buy/sell

in the said sectors. Details mentioned above are for

information purpose only.