Macro and

Equity Market

Outlook

Equity Market

Outlook

GLOBAL MACRO & MARKETS

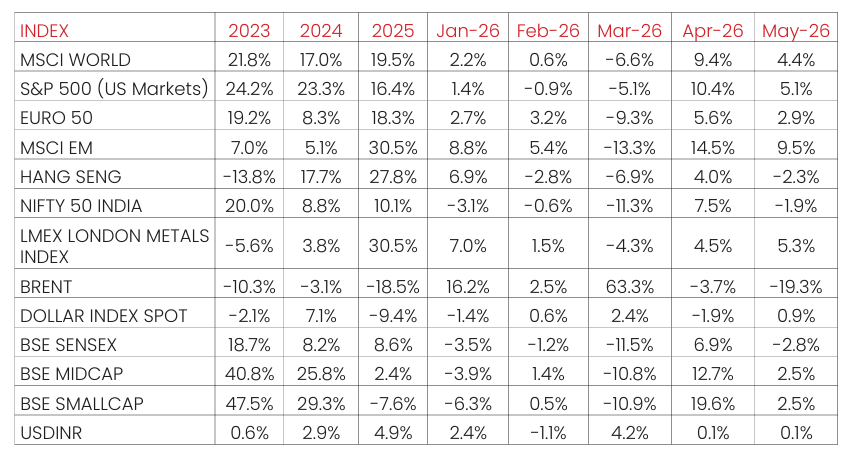

India’s NSE NIFTY 50 Index ended the month of May 2026 in red (-1.87%).

Among major global indices, the Japanese NIKKEI (+11.9%), Morgan

Stanley Capital International (MSCI) World (+4.4%), the Euro 50 (+2.9%)

and the S&P 500 (+5.1%) ended the month of May 2026 with positive

returns. Performance was mixed among Emerging Market (EM) indices in

May 2026, with the MSCI EM, Hang Seng, BOVESPA Brazil recording

sequential returns of (+9.5%), (-2.3%), and (-7.2%) respectively.

The London Metals Exchange (LME) Metals Index rose (+5.3%) in May 2026.

West Texas Intermediate (WTI) in red MoM, by (-16.9%) and Brent Crude

fell MoM, by (-19.3%), respectively, as markets remained cautious given

geopolitical uncertainty.

The Dollar Index rose by (+0.9%), through May 2026, with the US Dollar

(USD) appreciating vis-à-vis Emerging Market (EM) currencies (+0.8%) and

appreciating marginally against the Indian Rupee (INR) on the spot market

(+0.1%). Bond yields moved unevenly, with India’s 10Y G-Sec yields fell by

1.10 bps, while US 10Y G-Sec yields climbing 6.49 bps, and the German

Bund yield fell by -9.90 bps, with rates settling at 7.00%, 4.44% and 2.94%,

respectively.

Domestic Macro & Markets

The BSE SENSEX fell (-2.8%) in May 2026, in line with the NSE NIFTY Index.

The BSE Mid-Cap index & the BSE Small-Cap index outperformed the BSE

SENSEX, rising by (+2.5%) & (+2.5%), over the month of May 2026,

respectively. Sector-wise, Healthcare, Capital Goods and Metals were the

top outperformers over the month of May 2026, clocking (+4.9%), (+4.7%)

and (+3.7%) respectively. BSE Sensex’s 13 major sectoral indices posted

mixed performance in May 2026.

Net Foreign Institutional Investors (FII) flows into equities were negative

for May 2026 at (-$3.45 Bn), following (-$6.47 Bn) in April 2026. Domestic

Institutional Investors (DIIs) remained net buyers of Indian equities for the

33rd consecutive month with flows of +$8.67 Bn in May 2026 compared to

(+5.45 Bn) in April 2026.

India's high frequency data update:

Manufacturing PMI strengthened, GST collections remained robust on import

revenue, core sector and industrial output rebounded, credit growth stayed

elevated despite a slight moderation, while inflation edged higher and the

trade deficit widened.

Purchasing Managers’ Index Manufacturing PMI:

India’s Purchasing Managers’ Index Manufacturing (PMI) in May 2026 rose to

55.0 from 54.7 in April 2026, showing a clear improvement in operating

conditions after hitting a four year low in the month of March. The recovery

was driven by stronger demand, faster output growth, and rising export

orders, though cost pressure remained elevated.

Goods and Services Tax (GST) Collection:

Gross collections of INR 1.94 Tn (+3.3% YoY) in May 2026 the Gross

Domestic Revenue stood at Rs 1.35 lakh crore, down -2.6%, while Gross

Import Revenue stood at Rs 0.59 lakh crore, marking a sharp rise of 19.1%

during the month.

Core Sector Production:

The index of eight core sector industries grew (+1.7% YoY) in April 2026,

against a (-0.4% YoY) growth in March 2026. The production of Cement,

Steel and Electricity recorded growth in April 2026 by (+9.4% YoY), (+6.2%

YoY) and (+4.1% YoY) respectively.

Industrial Production:

Factory output growth as measured by the Index of Industrial Production

(IIP) grew YoY by (+4.9%) in April 2026, vs a growth of (+3.2%) YoY in March

2026. The growth rates of the Four sectors, Mining & Quarrying,

Manufacturing, Electricity & Gas Supply and Water Supply, Sewerage &

Waste Management for the month of April 2026 are (-5.1%), (+6.2%),

(+4.9%) and +(6.6%) respectively.

Credit growth:

Scheduled Commercial Bank Credit growth in May 2026 declined

marginally to (+16.2%) YoY vs (+16.6%) YoY in April 2026. Agriculture and

allied activities credit in April 2026 grew by (+13.7%) YoY, while industrial

sector credit grew by (+15.1%) YoY, the services sector credit grew by

(+18.6%) YoY.

Inflation:

Apr’26 Consumer Price Index (CPI) inflation rate accelerated YoY to 3.48%,

up from 3.40% in Mar’26. Food inflation accelerated YoY to 4.20%, up from

(+3.87%) in the previous month of Mar’26. The Wholesale Price Index (WPI)

inflation rose sequentially in Apr’26, with the print at (+8.30%) YoY,

Positive rate of inflation in April 2026 is primarily due to increase in prices

of mineral oils, crude petroleum & natural gas, basic metals, other

manufacturing and non-food articles etc.

Trade Deficit:

Indian Merchandise Exports rose by (+13.7%) YoY to $43.56 Bn in Apr

2026. Imports rose by (+10.0%) YoY to $71.94 Bn. Merchandise trade

deficit fell to (-$28.38) Bn, down from (-$20.7) Bn in March 2026 and

(-$27.10) Bn a year earlier.

Events to watch out for in June 2026

RBI MPC Meeting (June 3–5):

The Reserve Bank of India’s policy review is

the most direct domestic driver. With repo rates at 5.25%, the committee

faces a balancing act between sticky food inflation and slowing industrial

output. Any shift in tone on liquidity or growth projections will ripple

through bond yields, banking stocks, and credit markets.

Organization of the Petroleum Exporting Countries (OPEC+) (June 7):

Oil remains India’s largest import, and the OPEC+ meeting is crucial after

the UAE’s exit. Production quotas set by Saudi Arabia and Russia will

determine whether Brent crude stays above $100/bbl. For India, higher oil

prices mean pressure on the current account deficit, rupee depreciation,

and elevated inflation expectations. The seven participating countries

agreed to implement a production adjustment of 188,000 barrels per day

in June 2026, as part of the voluntary cuts announced in April 2023. These

adjustments may be phased out gradually or reversed depending on

market conditions, with countries reaffirming a cautious and flexible

approach to ensure oil market stability.

US Federal Open Market Committee (FOMC) (June 16–17):

The Fed’s

stance on interest rates will influence global capital flows. If hawkish,

emerging markets like India could see outflows, weakening the rupee and

raising borrowing costs. Conversely, a dovish tilt would support equity

inflows and ease pressure on yields. The Fed’s commentary on inflation

and growth may be closely tracked by Indian policymakers.

Other things to watch out for:

Beyond monetary policy, oil, Fed

decisions, and monsoon progress, other factors to watch in June 2026

include advance tax payments due mid month, which influence liquidity

flows; corporate earnings and IPO activity, and geopolitical tensions in the

Middle East and Europe, which could affect commodity prices and investor

sentiment. Together, these elements add layers of uncertainty and

opportunity for India’s economy in the near term. Geopolitical tensions

remain elevated, with the US–Israel-Iran conflict continuing to disrupt Gulf

shipping, alongside persistent uncertainties in Gaza and the ongoing

Russia-Ukraine war. These developments may be expected to weigh on

global trade flows and commodity markets through the quarter.

Monthly Performance for Key Indices:

Source:NIMF Research, Bloomberg, RBI

Note: Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Note: Market scenarios are not reliable indicators for current or future performance. The same should not be construed as investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Market View

Domestic equity markets continue to witness heightened volatility amid

persistent geopolitical tensions in West Asia, elevated crude oil prices, and

evolving global macroeconomic conditions. While markets have recovered

from the sharp correction seen earlier in the year, investor sentiment

remains cautious given the uncertainty surrounding energy prices, global

growth and capital flows.

Crude oil prices remain a key monitorable for India. Continued disruptions in

the Middle East and concerns around global energy supply have kept oil

prices elevated increasing risks to inflation, corporate profitability and

external balances. The duration and intensity of these geopolitical

developments will play an important role in determining the market

trajectory going forward.

The Indian Rupee has remained under pressure due to higher crude oil prices

and intermittent foreign capital outflows. However, India’s relatively strong

macroeconomic fundamentals and manageable external balances have

helped limit excessive currency volatility.

On the domestic front, economic growth remains resilient although the RBI

has marginally revised its growth outlook lower while raising its inflation

expectations to account for higher energy prices and global uncertainties.

Monetary policy remains supportive with the RBI maintaining a neutral

stance and keeping policy rates unchanged.

Following the market correction over the past several months valuations

have become more reasonable particularly within the large-cap segment.

While near-term earnings may face pressure from elevated input costs,

currency weakness and softer global demand the medium- to long-term

structural growth drivers for India remain intact.

Given geopolitical challenges and its implications, long term investments

may be invested systematically using the current corrective phase of the

market. Lack of visibility on impact of earnings due to crude oil, supply chain

challenges, currency depreciation are near term factors which may delay

recovery. Hence a systematic approach to adding allocations might help in

potentially lowering the anticipated volatility. The impact of war is visible on

select segments; delayed resolution could lead to downgrade in earnings.

Asset allocation in line with the risk appetite of the investor is an important

tool to navigate any unanticipated volatility. Accordingly Large Cap & Large

Cap oriented diversified strategies along with hybrid funds might appear to

be better placed on risk-reward basis, while Mid/Small cap allocation may be

considered in a staggered manner through systematic investment with a

long-term view.

Source:

NIMF Research,Bloomberg

Disclaimer:

The current fund philosophy may change in future depending on market conditions or fund manager’s views. The sectors mentioned

are not a recommendation to buy/sell in the said sectors. The scheme may or may not have future position in the said sectors. The

information herein above is meant only for general reading purposes and the views being expressed only constitute opinions and

therefore cannot be considered as guidelines, recommendations or as a professional guide for the readers. The document has been

prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. The

sponsors, the Investment Manager, the Trustee or any of their directors, employees, Associates or representatives (‘entities & their

Associate”) do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such information.

Recipients of this information are advised to rely on their own analysis, interpretations & investigations. Readers are also advised to

seek independent professional advice in order to arrive at an informed investment decision. Entities & the associates including

persons involved in the preparation or issuance of this material, shall not be liable in any way for any direct, indirect, special, incidental,

consequential, punitive, or exemplary damages, including on account of lost profits arising from the information contained in this

material. Recipient alone shall be fully responsible for any decision taken on the basis of this document.