Macro and

Equity Market

Outlook

Equity Market

Outlook

Global Macro & Markets

Persistently high inflation owing to seemingly prolonged

supply chain conundrums and resultant tightening worries have

impacted global equities and bonds alike. US 10Y is up 60bps

MoM and 202bps YTD. US Dollar index has strengthened 4.7% MoM.

LME Metals index had peaked in March and was down 6.6% over

the month. Amid weak global cues and probability of aggressive

rate hike by the US Fed, MSCI World Index fell 8.4% MoM. It

was dragged lower by S&P500 (-8.8%), NIKKEI (-3.5%) and

Euro-50 (-2.6%). NIFTY 50 India (-2.1%) outperformed other

major EMs (Emerging Markets). MSCI EM Index was down 5.7%,

wherein Brazil Bovespa, MOEX Russia & Hang Seng were down 10%,

9.6% and 4.1% respectively.

Domestic Macro & Markets

Indian markets have been buoyant and resilient since the

global markets recovered from the pandemic lows in last two

years. Broader markets outperformed the narrow index over the

month. BSE Midcap index and BSE Smallcap index were up 1.3%

and 1.4% MoM whereas SENSEX was down 2.6%. Among sector

indices, IT, Realty and Metals declined 12%, 4% and 3%

respectively, while utilities gained 18% during the month.

Market breadth declined in April with 42% of BSE 200 stocks

trading above their respective 200-day moving averages. FPIs

sold US$3.6 bn of Indian equities in the secondary market

while DIIs bought US$3.6 bn.

India's high frequency data update:

All-time high GST collections, strength within manufacturing

activity and rising exports bode well for the economy.

Manufacturing PMI:

Manufacturing PMI continued to remain expansionary at 54.7 in

April’22, quite better compared to 54 in March’22. Factories

continued to scale up production at an above-trend pace, with

ongoing increase in sales and input purchasing suggesting that

growth will be sustained in near-term.

GST Collection:

At INR 1.68 Tn (+20% YoY), collections in April’22 have marked

all-time high levels on the back of improved compliance,

enforcement action against tax evaders and pickup in economic

activity.

Core sector production:

Core sector production rose 4.3% YoY in March’22 as against a

YoY rise of 6% in February’22 and a rise of 12.6% same time

last year. On a sequential basis, infra output increased

14.6%.

Industrial Production:

Manufacturing IIP increased 0.8% in Feb’22 vs decline of 3.4%

in Feb last year.

Credit growth:

Credit growth accelerated to 10.1% YoY as of 8-Apr 2022

against YoY growth of 5.3% as observed on 9-Apr 2021.

Aggregate deposit growth also grew 10.1% YoY.

Inflation:

CPI inflation in March’22 shot up to 6.95% from 6.07% on the

back of sequentially higher food (+7.7%) and rural inflation

(+7.7%). WPI inflation increased 140bps to 14.5%.

Trade Deficit:

March’22 trade deficit widened to US$18.7 bn as compared to

US$21.2 bn in February’22. Exports increased 14.5% YoY to

US$40.4 bn while imports increased by 21% YoY to $59 bn.

Balance of Payments:

The current account registered a deficit of US$23 bn (2.7% of

GDP) in 3QFY22, widening from a deficit of US$9.9 bn in 2QFY22

(1.3% of GDP) and a deficit of US$2.2 bn in 3QFY21 (0.3% of

GDP). This was mainly due to a widening of the trade deficit

to US$60.4 bn (2QFY22: US$44.5 bn).

Fertilizer subsidy – revised:

The Cabinet increased the subsidy rate for Phosphatic and

Potassic (P&K) fertilizers under the Nutrient Based Subsidy

(NBS) scheme for the period April-September 2022. Rs 609 bn of

subsidy (for 1HFY23) was approved including support for

indigenous fertilizer (SSP) through freight subsidy and

additional support for indigenous manufacturing and imports of

Di-ammonium phosphate (DAP). Subsidy budgeted for P&K

fertilizers in FY2023 was Rs 420 bn.

Market View

Near term market sentiment is likely to be influenced by the

increased geopolitical risks in the backdrop of ongoing

Russia-Ukraine conflict, higher inflation/ commodity prices,

rate hikes by Global Central Banks and most importantly how

these factors impact the Global/domestic growth possibilities.

Accordingly, we anticipate higher than usual volatility or

market swings in the short term. From a domestic perspective

while direct impact of Russian-Ukraine conflict, through trade

channel may be limited, the indirect impact on Crude prices,

Inflation, rising input or raw material prices needs to be

monitored. Notwithstanding the short-term global risks and

assuming that the geo-political tensions are diffused soon, we

remain optimistic on a reasonable domestic recovery. Key

drivers include - relaxation of most COVID led restrictions

across states which may potentially spur demand, anticipated

revival in investment cycle & domestic manufacturing, etc.

Accordingly, we are attempting to maintain balanced portfolios

through a combination of domestic recovery themes along with

secular businesses. Given the external risks and its potential

impact we believe investing in a staggered manner or

systematic route may help iron out market extremes. Based on

the prevailing valuations diversified funds with allocations

across market cap range may be considered from a medium-term

view. Conservative investors seeking equity exposure with

lower volatility may consider asset allocation strategies like

- Balanced Advantage/Asset Allocator which manage equity

allocations dynamically.

Note:The sectors mentioned are not a

recommendation to buy/sell in the said sectors. The schemes

may or may not have future position in the said sectors. For

complete details on Holdings & Sectors of NIMF schemes, please

visit website mf.nipponindiaim.com;

Past performance may or may not be sustained in future

Past performance may or may not be sustained in future

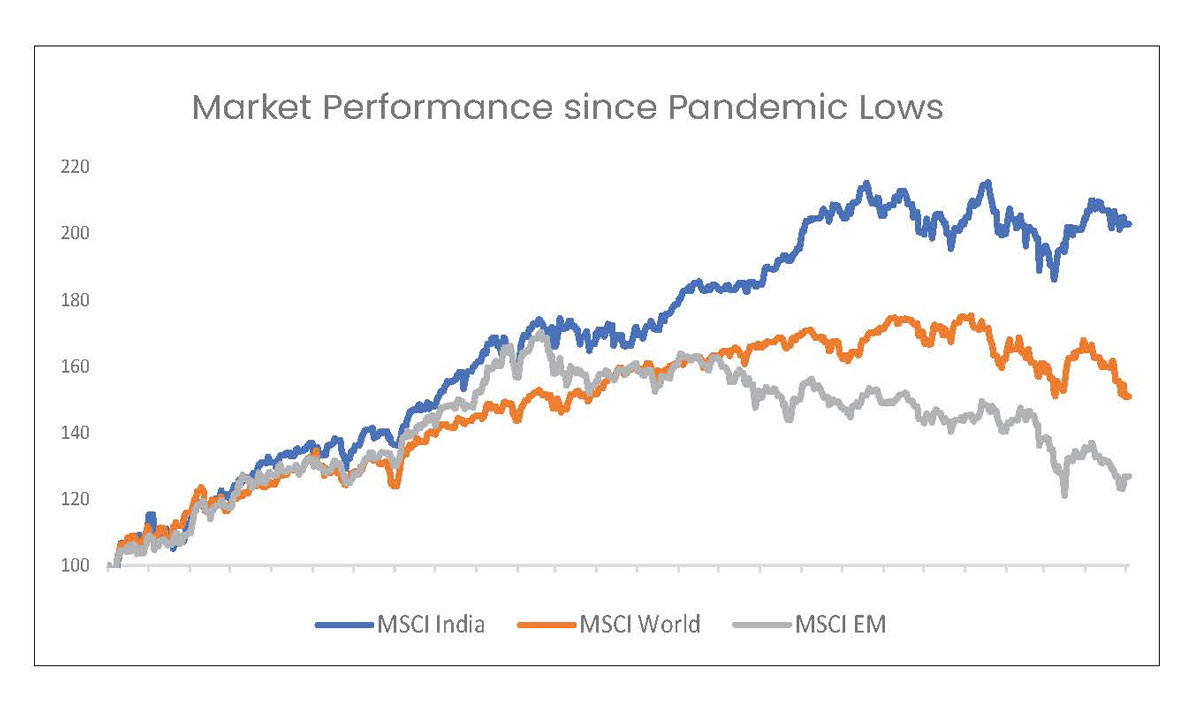

Chart of the month :

MSCI India has outperformed MSCI World and MSCI EM by 52% and

76% respectively since March 31, 2020 (25 months period).

Common Source:

Bloomberg, Nippon India Mutual Fund Research

Disclaimer:The information herein above is

meant only for general reading purposes and the views being

expressed only constitute opinions and therefore cannot be

considered as guidelines, recommendations or as a professional

guide for the readers. The document has been prepared on the

basis of publicly available information, internally developed

data and other sources believed to be reliable. The sponsors,

the Investment Manager, the Trustee or any of their directors,

employees, Associates or representatives (‘entities & their

Associate”) do not assume any responsibility for, or warrant

the accuracy, completeness, adequacy and reliability of such

information. Recipients of this information are advised to

rely on their own analysis, interpretations & investigations.

Readers are also advised to seek independent professional

advice in order to arrive at an informed investment decision.

Entities & their associates including persons involved in the

preparation or issuance of this material, shall not be liable

in any way for any direct, indirect, special, incidental,

consequential, punitive or exemplary damages, including on

account of lost profits arising from the information contained

in this material. Recipient alone shall be fully responsible

for any decision taken on the basis of this document. Budget

related information contained in this document is for general

purposes only and not a complete disclosure of every material

fact of the Indian Budget. For a detailed study, please refer

to the budget documents available on

http://www.indiabudget.gov.in