Macro and

Equity Market

Outlook

Equity Market

Outlook

GLOBAL MACRO &

MARKETS – October 2023

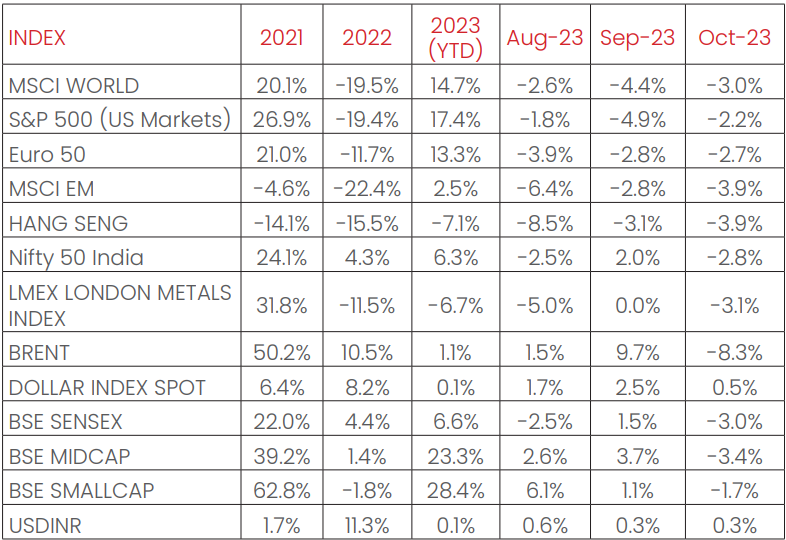

India’s NIFTY index ended the month in red, ending -2.8% MoM in

October. The S&P500 (-2.2%), the Euro 50 (-2.7%), the MSCI World

(-3.0%), Japan’s Nikkei (-3.1%) all ended the second consecutive

month in negative, as global markets remained volatile. Among the

emerging markets indices, the MSCI (Morgan Stanley Capital

International) EM, the HANG SENG, and BOVESPA Brazil corrected

marginally in October, by -3.9%, -3.9%, and -2.9% respectively. The

MOEX (Moscow Exchange) Russia bucked the negative trend, with

growth at +2.2% MoM (month on month).

LME (London Metal Exchange) Metals Index declined sequentially

by -3.1% in October, as China’s Manufacturing PMI (Purchasing

Manager's Index) slipped into contraction zone in October, coupled

with a stronger dollar. WTI (West Texas Intermediate) and Brent

Crude slipped in October, by -10.8% and -8.3% respectively, even as

the threat of supply side disruptions from the Israel- Hamas

conflict remained. The Dollar index strengthened by +0.5% through

October, with the Dollar depreciating by -0.2% vis-à-vis EM

currencies and appreciating by +0.3% against the Indian Rupee.

India 10Y G-Sec yields rose, rising by +14 bps, while US 10Y G-Sec

yield rose by +36 bps, and the German Bund yield fell by -3 bps,

with rates settling at 7.36%, 4.93% and 2.80% respectively. The surge

in yields of the US government bonds is a function of the

perception of high fiscal indebtedness of the US sovereign and a

recent pullback from foreign buyers.

Domestic Macro &

Markets - October 2023

The BSE SENSEX (-3.0%) fell in October, in tandem with other

benchmark Indian indices. BSE Mid-cap underperformed the

SENSEX and was down -3.4%. The BSE Small Cap index

outperformed, with a fall of -1.7% over the month. Sector-wise,

Realty, FMCG, Auto and consumer durables indices were the top 4

performers over the month, clocking +3.7%, -0.9%, -1.2%, and -2.3%,

respectively. The worst performing index was the BSE Power index,

which fell by -4.9%. Market breadth declined MoM, with stocks

trading above their respective 200-day moving averages

declining to 69% from 85% from September 2023, and the advance

decline line was down 11% MoM.

Net FII (Foreign Institutional Investors) flows into equities were

negative for October (-$2.6Bn, following -$1.8 Bn in September

2023). DIIs (Domestic Institutional Investors) remained net buyers of

Indian equities (+$3.4 Bn, from +$2.6 Bn from last month). YTD, FPI

net buying stands at US$12.1 Bn, while DIIs have bought stocks worth

US$19 Bn.

India's high frequency data update:

Elevated levels of GST collections, festive season demand uptick,

stable retail inflation, deflated input inflation, rising core sector

outputs, and elevated credit growth augurs well for the Indian

economy.

Manufacturing PMI (Purchasing Manager's Index):

Manufacturing PMI in October 2023 came in at 55.5, down from 57.5 in

September 2023, and remained in expansion zone (>50) for the 28th

straight month, as output expanded at the slowest level in 8 months

given a tepid rise in new orders, which fell to a 12-month low.

GST Collection:

Collections of INR 1.72 Tn (+13% YoY) in October 2023 concluded the

twentieth consecutive month of collections over the INR 1.4 Tn mark,

the second highest recorded since the inception of the regime,

following record collections of INR 1.87 Tn in April 2023. The average

monthly gross collection this fiscal year is INR 1.66 Tn. Rising

compliance, rising formalization of the economy, festive demand,

and improved administrative efficiency have driven sustainedly

high levels of GST collections.

Core sector production:

The index of eight core sector industries grew by 8.1% in September

2023, against an 12.1% jump in August 2023, as a favourable base

effect continued to come into play for India’s eight core sectors,

albeit at a slower pace. Seven of the constituent sectors recorded

positive YoY growths, with crude oil production declining by -0.4%.

Industrial Production:

Factory output as measured by the IIP index accelerated to a

14-month high of 10.3% in August 2023, vs a growth of 6% YoY in July

2023 (upwardly revised by 30 bps), buoyed by growths in all 3

constituent sectors- Mining, Manufacturing and Electricity.

Credit growth:

Scheduled Commercial Bank Credit growth reached 19.32% YoY as

of 6th October 2023 against YoY growth of 17.93% as observed on

7th October 2022.

Inflation:

September 2023 CPI (Consumer Price Index) inflation rate eased

below the RBI’s comfort zone of 6% for the first time in three months,

and reached 5.02%, easing from 6.83% in July 2023. Acceleration in

the CPI rate was attributed to a slowdown in the food basket

inflation, which came in at 6.56% in September 2023, compared to

the 9.94% rise in August 2023. WPI (Wholesale Price Index) inflation

remained in negative territory, with the September 2023 print at a

six-month high of -0.26%, 26 bps up from August’s at -0.52%, as

food, fuel and chemicals remained in the deflation zone.

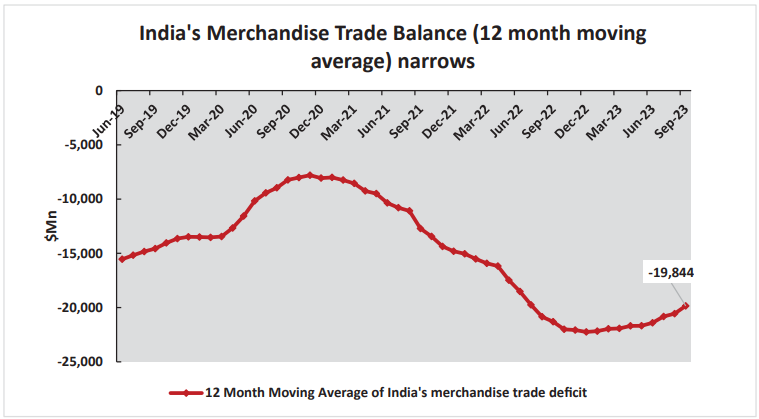

Trade Deficit:

Indian Merchandise Exports recorded a decline of -2.6% YoY to

$34.48 Bn in September 2023, while Imports growth declined by

-15.04% YoY to $53.84 Bn. India’s trade deficit narrowed $19.37 Bn as

the dollar strengthened.

Events that you may watch out for in November 2023:

War and Oil:

Further escalation of conflict between Israel and Hamas and the

risk of a contagion remain key monitorables for equity markets. Oil

supply side disruptions through war, coupled with supply cuts from

key producers Saudi Arabia and Russia may leave prices

vulnerable to elevated volatility.

Earnings season:

The ongoing Q2FY24 earnings season in India has been better than

expected, even as the market holds a cautious stance in terms of

price performances post announcements of results. Remaining

results may set the tone for Earnings revisions across the board for

Indian stocks.

State election outcomes:

Five states (Rajasthan, Chhattisgarh, Madhya Pradesh, Telangana,

and Mizoram) will head for polls in November 2023, as general

elections loom in early 2024. These elections may drive public

sentiment going into the Lok Sabha elections and remain a key

monitorable for equity markets.

Festive season demand:

November 2023 bodes well for India’s private consumption and

demand, as the festive season beckons, with Diwali commencing

an uptick in festive demand in the country.

Central Banks commentary:

While the US Federal Reserve (Fed) chose to hold interest rates on

November 1st 2023 for the second consecutive time at a 22-year

high level of 5.25-5.5%, the Bank of Japan widened their yield target

band, with 1% as a reference “upper band”, and 0% as a target yield

on their 10-year bond. The European Central Bank (ECB) decided to

hold rates steady after 10 consecutive hikes in October 2023. The

Reserve Bank of India (RBI) kept the key policy repo rate unchanged

at 6.5% in the October 2023 meet, holding rates constant for the 4th

consecutive time. Monetary policy commentaries were driven by

caution on energy and food inflation shocks, and decoupling in

policy stances may be seen in the coming months.

Monthly Performance for Key Indices:

Note: Market scenarios are not the reliable indicators for current or future

performance. The same should not be construed as

investment advice or as any research report/research recommendation.

Past performance may or may not be sustained in future.

Source: Bloomberg

Past performance may or may not be sustained in future.

Source: Bloomberg

Market View

Global economic trends remain mixed and challenging. The

geopolitical events in Israel -Gaza, US bond yields touching historic

highs and slowing growth in developed world etc, present

near-term headwinds.

On the positive India macros remains robust with strong

manufacturing growth, improving economic activity, slowing

inflation etc.

Local events like forthcoming state & general elections, global

developments like rising crude oil prices, mixed signals on global

growth etc appears to be ignored in the current euphoria. Large

Caps appear to be better positioned on a relative basis and along

with Asset Allocation products like Multi Asset Funds, Balanced

Advantage etc may assist to manage the near term risks. Investors

apprehensive of the equity market swings can consider

participating in a staggered manner in line with their risk appetite

and investment goals.

Note: The sectors mentioned are not a recommendation to buy/sell in the said sectors.

The schemes may or may not have future

position in the said sectors. For complete details on Holdings & Sectors of NIMF schemes, please visit

website mf.nipponindiaim.com.

Past performance may or may not be sustained in future

Past performance may or may not be sustained in future

Chart of the month :

India’s trade deficit narrowed to USD -19.37 Bn in September 2023,

as imports fell faster than exports, and the trend of the deficit

narrowed (12 Month Moving average), pointing at improving

economic fundamentals.

Common Source:

NIMF Research, CEIC, Bloomberg

Disclaimer: The information herein above is meant only for general reading purposes

and

the views being expressed only

constitute opinions and therefore cannot be considered as guidelines, recommendations or as a

professional guide for

the readers. The document has been prepared on the basis of publicly available information, internally

developed data

and other sources believed to be reliable. The sponsors, the Investment Manager, the Trustee or any of

their directors,

employees, Associates or representatives (‘entities & their Associate”) do not assume any

responsibility

for, or warrant the

accuracy, completeness, adequacy and reliability of such information. Recipients of this information

are

advised to rely on

their own analysis, interpretations & investigations. Readers are also advised to seek independent

professional advice in

order to arrive at an informed investment decision. Entities & their associates including persons

involved in the preparation

or issuance of this material, shall not be liable in any way for any direct, indirect, special,

incidental, consequential, punitive

or exemplary damages, including on account of lost profits arising from the information contained in

this material.

Recipient alone shall be fully responsible for any decision taken on the basis of this document.