What do you usually do when you receive your annual bonus? Keep it aside for some future goal, preserve it in traditional investment instruments, or use it for pre-payment of some loan, right? What if there was an option to park this money for a short term of three to six months? And what if you could earn returns from such an investment? Sounds fantastic, doesn’t it? Well, well. Here is a parking spot for your surplus funds that could be both easy to access and beneficial. Ultra-Short-Term Funds/ Ultra Short Duration Funds.

What are Ultra Short Duration Funds?

Ultra-Short-Term Fund is a type of debt mutual fund that invests in securities with a maturity of three to six months. These funds are open-ended debt schemes, meaning investors can invest and withdraw their funds in these schemes any time they want. This is unlike close-ended schemes where investors can enter or exit the scheme only during specific periods. Therefore, transacting in ultra-short-term funds can be easy and convenient.

Another reason why accessing funds from Ultra Short Duration Fund investment can be easy is because these schemes aim to invest in highly liquid debt instruments such as treasury bills, money market instruments, commercial papers, certificates of deposits, etc. Now that you have understood the basics of ultra-short-term debt funds, let’s look at how these funds work.

How do Ultra Short-term Mutual Funds work?

இந்தியாவில் உள்ள அனைத்து மியூச்சுவல் ஃபண்டுகளையும் போலவே, அதிக குறுகிய கால மியூச்சுவல் ஃபண்டுகள் இந்திய பத்திரங்கள் மற்றும் பரிமாற்ற வாரியம் (SEBI) மூலம் ஒழுங்குபடுத்தப்பட்டு கண்காணிக்கப்படுகின்றன. SEBI மூலம் அமைக்கப்பட்ட விதிகள், ஒழுங்குமுறைகள் மற்றும் வழிகாட்டுதல்கள் முதலீட்டில் வெளிப்படைத்தன்மையை உறுதி செய்கின்றன மற்றும் முதலீட்டாளர்களின் நலன்களை பாதுகாக்க உதவுகின்றன.

SEBI விதிகளின்படி, இந்த திட்டங்கள் முதன்மையாக 3-6 மாதங்கள் மெச்சூரிட்டியுடன் கடன் பத்திரங்களில் முதலீடு செய்கின்றன. இந்த குறைந்த மெச்சூரிட்டி காரணமாக, குறுகிய கால நிதிகளில் முதலீடுகள் குறைந்த ஆபத்து என்று கருதப்படலாம். குறைந்த-ஆபத்து முதலீட்டிற்கான மற்றொரு காரணம் என்னவென்றால், இந்த நிதிகளின் அடிப்படை பத்திரங்கள் தனியார் நிறுவனங்களின் பங்குகள் அல்லது ஈக்விட்டிகளில் முதலீடு செய்வதை விட ஒப்பீட்டளவில் குறைவான நிலையற்றவை என்பதாகும்.

அல்ட்ரா ஷார்ட் டேர்ம் ஃபண்ட்ஸ் திட்டங்களில் முதலீடு மீதான வருமானங்கள் நிகர சொத்து மதிப்பு (என்ஏவி)-யில் நிதியின் மாற்றத்தின் அடிப்படையில் கணக்கிடப்படுகின்றன, இது சந்தையில் நடைமுறையிலுள்ள வட்டி விகிதங்களின் அடிப்படையில் ஏற்ற இறக்கமாகும். இருப்பினும், நிலையான மெச்சூரிட்டியுடன் மூலதனம் கருவிகளுக்கு அம்பலப்படுத்தப்படுவதால் இந்த நிதிகளால் உருவாக்கப்பட்ட வருமானங்களை கணிக்க முடியும்.

லிக்விட் ஃபண்டு மற்றும் அல்ட்ரா-ஷார்ட் டியூரேஷன் ஃபண்டு இடையேயான வேறுபாடு

அல்ட்ரா ஷார்ட்-டேர்ம் ஃபண்டுகள் என்பது 3-6 மாதங்கள் மெச்சூரிட்டி கொண்ட பத்திரங்களில் முதலீடு செய்யும் கடன் திட்டங்கள் ஆகும். மறுபுறம், லிக்விட் ஃபண்டுகள், குறுகிய மெச்சூரிட்டிகளுடன் கூட பத்திரங்களில் முதலீடு செய்வதை நோக்கமாகக் கொண்டுள்ளன. பெயர் குறிப்பிடுவது போல், திரவ நிதிகளின் முதன்மை நோக்கம் பணப்புழக்கத்தை வழங்குவதாகும், அதாவது முதலீட்டாளர்களுக்கு நிதிகளை எளிதாக அணுகுவதாகும். எனவே, லிக்விட் மியூச்சுவல் ஃபண்டுகள் பொதுவாக 91 நாட்கள் வரை மெச்சூரிட்டியுடன் கடன் பத்திரங்களில் முதலீடு செய்கின்றன. அடிப்படை பத்திரங்களின் மெச்சூரிட்டி காலத்தைத் தவிர, லிக்விட் ஃபண்டுக்கும் அதிக குறுகிய கால நிதிக்கும் இடையே பெரும் வேறுபாடு இல்லை. வரிவிதிப்பு விதிகள் இரண்டு கடன் திட்டங்களுக்கும் ஒரே மாதிரியானவை. முதலீட்டாளர்கள் தங்கள் முதலீட்டு நோக்கம் மற்றும் கிடைமட்டத்திற்கு ஏற்ற நிதியை தேர்ந்தெடுக்க வேண்டும்.

நீங்கள் ஏன் அல்ட்ரா-ஷார்ட்-டியூரேஷன் ஃபண்டுகளில் முதலீடு செய்ய வேண்டும்?

● எளிதான பணப்புழக்கம்

பாரம்பரிய முதலீட்டு முறைகளைப் போலல்லாமல், முன்கூட்டியே நிதிகளை திரும்பப் பெறுவதற்கான அபராதம் இருக்கும் நிலையில், அதிக குறுகிய கால மியூச்சுவல் ஃபண்டுகள் அவற்றுடன் ஒப்பிடும்போது உயர்ந்த மற்றும் எளிதான பணப்புழக்கத்தை வழங்குகின்றன. இந்த நிதிகள் எந்தவொரு லாக்-இன் காலத்தையும் கொண்டுள்ளன மற்றும் குறுகிய காலத்தில் மிகவும் சிறந்த வருமானத்தை வழங்குவதை நோக்கமாகக் கொண்டுள்ளன.

● குறைந்த-ஆபத்து முதலீடு

மேலே குறிப்பிட்டுள்ளபடி, கருவூலப் பத்திரங்கள், அரசாங்கப் பத்திரங்கள், வணிகப் பத்திரங்கள் போன்ற கடன் பத்திரங்களில் அதி-குறுகிய-கால நிதிகள் முதலீடு செய்கின்றன. அவை ஒப்பீட்டளவில் நிலையான கருவிகள் மற்றும் ஒப்பீட்டளவில் ஈக்விட்டியுடன் ஒப்பிடுகையில் குறைந்த ஏற்றத்தாழ்வுகள் ஆகும். மேலும், பத்திரங்களின் குறைந்த ஹோல்டிங் காலம் வட்டி விகித அபாயம், கால ஆபத்து அல்லது கடன் ஆபத்து போன்ற பிற அபாயங்களுக்கு உங்கள் வெளிப்பாட்டை குறைக்கிறது.

● சிறந்த வருவாய்களின் சாத்தியக்கூறு

அல்ட்ரா-ஷார்ட்-டேர்ம் மியூச்சுவல் ஃபண்டுகளால் உருவாக்கப்பட்ட வருமானங்கள் உத்தரவாதமளிக்கப்படவில்லை என்றாலும், பாரம்பரிய முதலீட்டு கருவிகளை விட அவை ஒப்பீட்டளவில் சிறந்த மற்றும் அதிக கணிக்கக்கூடிய வருமானங்களை வழங்குவதை உறுதி செய்கின்றன.

அல்ட்ரா-ஷார்ட் கால கடன் நிதிகளின் வரிவிதிப்பு

கடன் மியூச்சுவல் ஃபண்டுகள் குறுகிய கால நிதிகள் என்பதால், இந்த திட்டங்களுக்கு கடன் வகைகளின் வரிவிதிப்பு விதிகள் பயன்படுத்தப்படுகின்றன. இதன் பொருள் நீங்கள் 36 மாதங்கள் வரை அதிக குறுகிய-கால நிதியில் முதலீட்டை வைத்திருந்தால், முதலீட்டில் சம்பாதித்த வருமானம் குறுகிய-கால மூலதன ஆதாயமாக கருதப்படும் மற்றும் உங்கள் வரிக்கு உட்பட்ட வருமானத்தில் சேர்க்கப்படும். இந்த லாபங்கள் உங்கள் அந்தந்த வரி வரையறை விகிதத்தின்படி வரி விதிக்கப்படும்.

உங்கள் அல்ட்ரா குறுகிய-கால கடன் நிதி முதலீடு 36 மாதங்களுக்கும் மேலாக நடத்தப்பட்டால், லாபங்கள் நீண்ட-கால மூலதன லாபங்களாக கருதப்படும். அனைத்து கடன் மியூச்சுவல் ஃபண்டுகளுக்கும் குறியீடு செய்த பிறகு அத்தகைய லாபங்களுக்கு 20% வரி விதிக்கப்படுகிறது. எனவே, அல்ட்ரா-ஷார்ட்-டேர்ம் திட்டங்களில் நீண்ட-கால முதலீடு உங்களுக்கு குறியீட்டு நன்மைகளை பெற உதவும் .

இருப்பினும், 1 ஏப்ரல் 2023 முதல், நிதி பில் 2023 குறிப்பிட்ட மியூச்சுவல் ஃபண்ட் திட்டங்களில் செய்யப்பட்ட முதலீட்டிற்கான நீண்ட கால மூலதன ஆதாயத்தில் குறியீட்டு நன்மையை அகற்றியுள்ளது. அத்தகைய சூழ்நிலையில், எந்தவொரு மூலதன ஆதாயங்களும் இயற்கையில் குறுகிய காலமாக கருதப்படும் மற்றும் ஹோல்டிங் காலம் எதுவாக இருந்தாலும் முதலீட்டாளரின் பொருந்தக்கூடிய வரி விகித வரம்பின்படி வரி விதிக்கப்படும். இந்த ஏற்பாடு 1 ஏப்ரல் 2023 அன்று அல்லது அதற்கு பிறகு செய்யப்பட்ட எந்தவொரு புதிய முதலீடுகளுக்கும் மட்டுமே பொருந்தும்.

“Specified Mutual Fund” means a Mutual Fund scheme which does not invest more than 35% in equity shares of domestic companies.

அல்ட்ரா-ஷார்ட்-டியூரேஷன் ஃபண்டுகளில் யார் முதலீடு செய்ய வேண்டும்?

சில மாதங்கள் குறுகிய காலத்திற்கு ஒரு மொத்த தொகையை நிறுத்த விரும்பும் முதலீட்டாளர்கள் அல்லது கடன் கருவியில் பணத்தை முதலீடு செய்ய விரும்புபவர்கள் அதி-குறுகிய-கால மியூச்சுவல் ஃபண்டுகளில் முதலீடு செய்வதை கருத்தில் கொள்ளலாம். இந்த திட்டங்கள் சிறிய முதலீட்டு வரம்பு கொண்ட முதலீட்டாளர்களுக்கு பொருத்தமானவை.

எஸ்டிபி (சிஸ்டமேட்டிக் டிரான்ஸ்ஃபர் திட்டம்) வசதியை தேர்வு செய்யும் முதலீட்டாளர்களுக்கும் அல்ட்ரா-ஷார்ட்-டேர்ம் ஃபண்டுகள் பொருத்தமானவை. ஒரு மியூச்சுவல் ஃபண்ட் திட்டத்திலிருந்து மற்றொரு தொகைக்கு ஒரு குறிப்பிட்ட தொகையை டிரான்ஸ்ஃபர் செய்ய எஸ்டிபி உங்களை அனுமதிக்கிறது.

எடுத்துக்காட்டாக, நீண்ட காலத்திற்கு முதலீடு செய்ய உங்களிடம் ஒரு மொத்த தொகை இருந்தால், அதை ஒரே நேரத்தில் ஈக்விட்டி ஃபண்டில் வைப்பதற்கு பதிலாக, நீங்கள் அந்தத் தொகையை அதி-குறுகிய-கால நிதியில் முதலீடு செய்யலாம் மற்றும் எஸ்டிபி-ஐ அட்டவணையிடலாம், இது உங்களுக்கு விருப்பமான ஈக்விட்டி திட்டத்திற்கு அவ்வப்போது ஒரு நிலையான தொகையை டிரான்ஸ்ஃபர் செய்யும். இந்த வழியில், நீங்கள் ரூபாய் செலவை சராசரியாக பெறலாம் மற்றும் கடன் மற்றும் ஈக்விட்டி திட்டங்களில் முதலீட்டில் வருமானத்தை சம்பாதிக்கலாம்.

அல்ட்ரா-ஷார்ட்-டியூரேஷன் ஃபண்டுகளில் முதலீடு செய்யும்போது கருத்தில் கொள்ள வேண்டிய காரணிகள்

● தொடர்புடைய ஆபத்து

கடன் மியூச்சுவல் ஃபண்ட் முதலீட்டில் உள்ள அடிப்படை கருத்துக்களில் ஒன்று அடிப்படை பத்திரங்களை வைத்திருப்பதற்கான காலம் நீண்டதாகும், வட்டி விகித இயக்கத்தால் எதிர்மறையாக பாதிக்கப்படும் முதலீட்டு வாய்ப்புகள் அதிகமாக இருக்கும். இது கால ஆபத்து என்று அழைக்கப்படுகிறது. எனவே, நீண்ட மெச்சூரிட்டி காலங்களுடன் கடன் முதலீடுகள் வட்டி விகித சுழற்சியால் பாதிக்கப்படும்.

மேலும், அதி குறுகிய கால மியூச்சுவல் ஃபண்டுகளில் முதலீடு செய்யும் போது கடன் அபாயத்தின் ஒரு கூறுபாடு கருதப்பட வேண்டும். நிதி மேலாளரில் நிதி போர்ட்ஃபோலியோவில் குறைந்த கடன் மதிப்பிடப்பட்ட கருவிகள் இருந்தால், இந்த நிதியில் உங்கள் முதலீடு கிரெடிட் ஆபத்துக்கு ஆளாகிறது.

● திட்டத்தின் பதிவை கண்காணிக்கவும்

அதன் கடந்த கால செயல்திறன் அடிப்படையில் மியூச்சுவல் ஃபண்ட் திட்டத்தில் முதலீடு செய்யத் தொடங்குவது புத்திசாலித்தனம் அல்ல. எவ்வாறெனினும், நிதி நிர்வாகத்தின் கண்காணிப்பு பதிவின் அடிப்படையில் ஒரு திட்டத்தை மதிப்பீடு செய்வது ஒரு நல்ல நடைமுறையாக இருக்கலாம். பல்வேறு பொருளாதார சுழற்சிகளில் நிதி எவ்வாறு செயல்பட்டுள்ளது என்பதை சரிபார்க்கவும். திட்டத்தின் டிராக் பதிவை சரிபார்ப்பது மற்றும் நிதி நிறுவனம் உங்கள் முதலீடு நம்பகமான அல்ட்ரா-ஷார்ட்-டேர்ம் கடன் நிதியில் இருப்பதை உறுதி செய்யும்.

● முதலீட்டு நோக்கம் மற்றும் தவணைக்காலம்

முதலீட்டு இலக்குகள் மற்றும் கிடைமட்டத்தை கருத்தில் கொண்டு எந்த முதலீடும் இருந்தாலும் அது மிகவும் முக்கியத்துவம் வாய்ந்தது. உங்கள் முதலீட்டு வரம்பு ஒரு வருடத்திற்கும் குறைவாக இருந்தால், நிப்பான் இந்தியா அல்ட்ரா-ஷார்ட் டியூரேஷன் ஃபண்ட் போன்ற அல்ட்ரா-ஷார்ட்-டேர்ம் ஃபண்டுகளில் முதலீடு செய்வது விவேகமானது.

● நிதி மேலாண்மை/ செலவு விகிதத்தின் செலவு

ஒவ்வொரு மியூச்சுவல் ஃபண்டும் செலவு விகிதம் என்றும் அழைக்கப்படும் ஒரு குறிப்பிட்ட நிதி மேலாண்மை கட்டணத்தை கொண்டுள்ளது . SEBI விதிமுறைகள் இந்த கட்டணத்தை 1.05% என்ற எண்ணில் வரம்பு வைத்திருந்தாலும், இது எந்தவொரு அதி-குறுகிய-கால கடன் நிதியிலும் முதலீடு செய்வதற்கு முன்னர் கருதப்பட வேண்டிய ஒரு முக்கியமான காரணியாகும். திட்டத்தின் செலவு விகிதம் குறைவாக இருந்தால், சற்று அதிக வருமானங்கள் உங்கள் போர்ட்ஃபோலியோவில் பிரதிபலிக்கப்படலாம்.

அல்ட்ரா ஷார்ட்-டேர்ம் மியூச்சுவல் ஃபண்டுகளில் எவ்வாறு முதலீடு செய்வது?

அல்ட்ரா-ஷார்ட்-டேர்ம் மியூச்சுவல் ஃபண்டுகளில் முதலீடு செய்ய நீங்கள் ஒட்டுமொத்த தொகை முதலீட்டு முறையை அல்லது எஸ்ஐபி முறையான முதலீட்டு திட்டத்தை* தேர்வு செய்யலாம். இந்த திட்டங்களில் முதலீடு செய்வதற்கு உயர் வரம்பு இல்லை, மேலும் நீங்கள் குறைந்தபட்சம் ரூ. 500 உடன் தொடங்கலாம். இப்போது முதலீடு செய்ய, எங்கள் நிப்பான் இந்தியா அல்ட்ரா ஷார்ட் டியூரேஷன் ஃபண்டு பக்கத்தை அணுகவும்.

எந்தவொரு ஏஎம்சி-யின் இணையதளம் அல்லது முதலீட்டு போர்ட்டல்கள் மூலம் அதிக குறுகிய-கால நிதியில் நீங்கள் எளிதாக முதலீடு செய்ய தொடங்கலாம். உங்கள் KYC சரிபார்ப்பு முடிந்தவுடன், முதலீடு செய்ய தொடங்குவது ஒரு எளிய, தொந்தரவு இல்லாத செயல்முறையாகும். ஆன்லைன் தளங்களுடன், இப்போது உங்கள் முதலீட்டை கண்காணிக்கவும் ரெடீம் செய்யவும் மிகவும் எளிதானது.

கீழே உள்ள வரி என்னவென்றால், உங்கள் உபரியை நிறுத்த அல்லது குறுகிய காலத்திற்கு நிலையான மற்றும் பாதுகாப்பான கருவியில் முதலீடு செய்ய நீங்கள் குறைந்த-ஆபத்து முதலீட்டு விருப்பத்தை தேடுகிறீர்கள் என்றால், அல்ட்ரா-ஷார்ட்-டேர்ம் ஃபண்டுகள் சரியான தேர்வாக இருக்கலாம்.

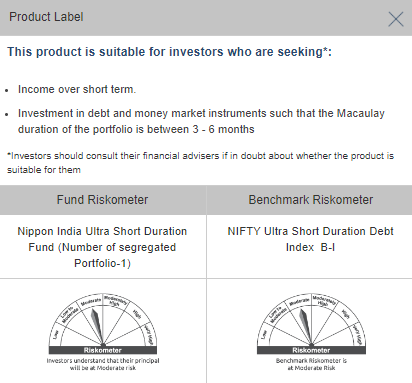

தயாரிப்பு லேபிள்

*எஸ்ஐபி என்பது சிஸ்டமேட்டிக் முதலீட்டுத் திட்டத்தை குறிக்கிறது, இதில் நீங்கள் ஒரு நிலையான தொகையை கால இடைவெளியில் முதலீடு செய்யலாம் மற்றும் கூட்டு அதிகாரத்தின் மூலம் சிறந்த நன்மைகளை நோக்கமாகக் கொண்டுள்ளீர்கள்.

பொறுப்புத்துறப்பு:

இங்குள்ள தகவல் பொதுவான வாசிப்பு நோக்கங்கள் மற்றும் கருத்துக்களை மட்டுமே வெளிப்படுத்துகின்றன மற்றும் எனவே வாசகர்களுக்கான வழிகாட்டுதல்கள், பரிந்துரைகள் அல்லது ஒரு தொழில்முறை வழிகாட்டியாக கருதப்பட முடியாது. இந்த ஆவணம் பொதுவாக கிடைக்கக்கூடிய தகவல், உள்நாட்டில் உருவாக்கப்பட்ட தரவு மற்றும் பிற நம்பக்கூடிய ஆதாரங்கள் மூலம் உருவாக்கப்பட்டுள்ளது. ஸ்பான்சர், முதலீட்டு மேலாளர், டிரஸ்டி அல்லது அவர்களின் இயக்குனர்கள், ஊழியர்கள், சங்கங்கள் அல்லது பிரதிநிதிகள் ("நிறுவனங்கள் மற்றும் அவர்களின் சங்கங்கள்") அத்தகைய தகவலின் துல்லியம், முழுமை, போதுமான மற்றும் நம்பகத்தன்மைக்கான எந்தவொரு பொறுப்பையும் ஏற்க மாட்டார்கள். இந்த தகவலின் பெறுநர்கள் தங்கள் சொந்த பகுப்பாய்வு, விளக்கங்கள் மற்றும் விசாரணைகளை நம்புமாறு அறிவுறுத்தப்படுகிறார்கள். தகவலறிந்த முதலீட்டு முடிவை எடுப்பதற்காக வாசகர்களுக்கு சுயாதீனமான தொழில்முறை ஆலோசனையை தேடுமாறும் அறிவுறுத்தப்படுகிறது. இந்த மெட்டீரியலின் தயாரிப்பு அல்லது வழங்குதலில் ஈடுபட்டுள்ள நபர்கள் உட்பட நிறுவனங்கள் மற்றும் அவர்களின் துணை நிறுவனங்கள் இந்த மெட்டீரியலில் உள்ள தகவலில் இருந்து ஏற்படும் இழந்த இலாபங்கள் உட்பட எந்தவொரு நேரடி, மறைமுக, சிறப்பு, தற்செயலான, விளைவான, தண்டனைக்குரிய அல்லது உதாரணமான சேதங்களுக்கும் எந்தவொரு வழியிலும் பொறுப்பேற்காது. இந்த ஆவணத்தின் அடிப்படையில் எடுக்கப்பட்ட எந்தவொரு முடிவுக்கும் பெறுநர் மட்டுமே முழுமையாக பொறுப்பாளியாக இருப்பார்.

மியூச்சுவல் ஃபண்டு முதலீடுகள் சந்தை அபாயங்களுக்கு உட்பட்டவை, திட்டம் சார்ந்த அனைத்து ஆவணங்களையும் கவனமாகப் படிக்கவும்.